Section One — Most Serious Problems

334

A Proactive Approach to Developing a Government-Issued Debit Card

to Receive Tax Refunds Will Benefit Unbanked Taxpayers

Legislative

Recommendations

Most Serious

Problems

Most Litigated

Issues

Case Advocacy Appendices

MSP #19

MSP

#19

A Proactive Approach to Developing a Government-Issued Debit

Card to Receive Tax Refunds Will Benefit Unbanked Taxpayers

RESPONSIBLE OFFICIALS

Beth Tucker, Deputy Commissioner for Operations Support

Jodi Patterson, Director, Return Integrity and Correspondence Services

Peggy Bogadi, Commissioner, Wage and Investment Division

DEFINITION OF PROBLEM

At least 17 million U.S. adults are unbanked, lacking any type of bank account, while 51

million others are underbanked.

1

Unbanked taxpayers have no free option to electronically

receive their tax refunds — i.e., returns of their tax overpayments or other congressionally-

authorized benefit transfers. For example, nearly 56 percent of the unbanked population

and 18 percent of the underbanked population (amounting to over 19 million individual

taxpayers) have a household income of less than $15,000, and receive an average refund of

almost $1,250.

2

The Treasury Department attempted to address this problem in the 2011 filing season

when it launched a debit card pilot program to issue refunds via prepaid cards to more

than 800,000 unbanked or underbanked taxpayers.

3

After analyzing the preliminary results

of the pilot, Treasury decided to end the program due to low participation rates.

4

Yet, the

design of the pilot may have caused the low participation. By evaluating the methodology

of the pilot, with particular focus on the findings and conclusions of the Urban Institute,

the IRS could develop a more effective strategy for a future debit card program.

5

The National Taxpayer Advocate believes it is in the best interest of taxpayers and tax ad-

ministration to make a government-sponsored tax refund debit card available nationwide.

Treasury already uses the Direct Express Debit MasterCard to distribute federal benefits

such as Social Security payments. In fact, more than 90 government-funded benefit pro-

grams already use some form of prepaid card.

6

1

Federal Deposit Insurance Corporation (FDIC), 2011 FDIC National Survey of Unbanked and Underbanked Households, Executive Summary 4 (Sept.

2012).

2

FDIC, 2011 FDIC National Survey of Unbanked and Underbanked Households 23 (Sept. 2012)(Actual numbers were 55.8 percent of unbanked and 17.5

percent of underbanked). Refunds for all taxpayers with $15,000 or less total positive income averaged $1,247, with a median refund of $539. IRS

Compliance Data Warehouse, Tax Year 2010, Individual Returns Transaction File.

3

“Unbanked” taxpayers have no checking or savings accounts. “Underbanked” taxpayers have a checking or savings account but rely on alternative financial

services, such as commercial check cashing services, refund anticipation loans, pawnshops, and money orders. Caroline Ratcliffe, Signe-Mary McKernan,

Urban Institute, Tax Time Account Direct Mail Pilot Evaluation ES-1 (Sept. 2012).

4

Eric Kroh, Treasury Won’t Renew Debit Card Refund Program in 2012, Spokesman Confirms, Tax Notes Today (Nov. 1, 2011).

5

Caroline Ratcliffe, Signe-Mary McKernan, Urban Institute, Tax Time Account Direct Mail Pilot Evaluation (Sept. 2012).

6

See http://www.fms.treas.gov/directexpresscard/index.html (last visited Sept. 9, 2012); Caroline Ratcliffe, Signe-Mary McKernan, Urban Institute, Tax Time

Account Direct Mail Pilot Evaluation 3 (Sept. 2012).

Taxpayer Advocate Service — 2012 Annual Report to Congress — Volume One

335

MSP #19

A Proactive Approach to Developing a Government-Issued Debit Card

to Receive Tax Refunds Will Benefit Unbanked Taxpayers

Legislative

Recommendations

Most Serious

Problems

Most Litigated

Issues

Case AdvocacyAppendices

Most Serious Problem

In addition, the National Taxpayer Advocate remains concerned about the incorporation of

the existing Western Union MoneyWise prepaid card into the TaxWise preparation soft-

ware used at most Volunteer Income Tax Assistance (VITA) sites. The IRS has partnered

with several financial institutions to offer refunds on debit cards offered by VITA and Tax

Counseling for the Elderly (TCE) organizations, but claims it does not endorse any particu-

lar product. However, the IRS provides volunteer sites with free CCH TaxWise software,

which incorporates a Western Union debit card product, and the terms associated with this

particular product appear less favorable than for other products.

7

The National Taxpayer

Advocate requested a copy of the contract from the IRS, but the IRS declined to provide

her with a copy of the contract unless CCH/TaxWise consented pursuant to an exemption

to the Freedom of Information Act. The National Taxpayer Advocate plans to review the

contract to effectively discharge her statutory tax administration duties.

8

ANALYSIS OF PROBLEM

A Government-Sponsored Nationwide Debit Card Program for Tax Refunds Would

Benefit Both Taxpayers and Tax Administration.

A nationwide debit card program to distribute tax refunds benefits both unbanked taxpay-

ers and the government.

9

Taxpayers would benefit in the following ways:

Quick Refund Turnaround and Minimal Cost. An electronic refund (coupled with

electronic filing) is the fastest refund delivery mechanism. Direct deposit is an ideal

method of receipt, with no cost to the taxpayer. Unbanked taxpayers cannot benefit

from the use of direct deposit and consequently have no way to receive refunds elec-

tronically, quickly, and free. As a result, they must either wait longer to receive refunds

by paper check, and potentially incur high check-cashing fees, or purchase a high-cost

commercial refund delivery product. If the system were planned properly, taxpayers

would not incur high fees to access funds deposited onto a government-sponsored

debit card.

To illustrate the importance of quick refund turnaround and low cost access to

refunds, it is necessary to understand the financial status of the unbanked and

7

Western Union MoneyWise Prepaid MasterCard Overview, http://cchsfs-taxwise.custhelp.com/app/answers/detail/a_id/382/~/western-union-mon-

eywise-prepaid-mastercard-overview (last visited Sept. 9, 2012); Government Accountability Office (GAO), GAO-11-481, 2011 Tax Filing: IRS Dealt with

Challenges to Date but Needs Additional Authority to Verify Compliance 38 (Mar. 2011).

8

The Freedom of Information Act (FOIA) is a law ensuring public access to U.S. government records. 5 U.S.C. § 552. However, the Act provides several

exemptions to the general presumption of mandatory disclosure. Section 552(b)(4) exempts from disclosure “[t]rade secrets and commercial or financial

information obtained from a person and privileged or confidential.” IRM 11.3.13.9.2(8) (Jan. 1, 2006) provides “Contracts and related records, including

evaluative records, concerning the purchase of goods and services are agency records, but they may contain trade secrets and commercial or financial

information which is privileged or confidential. Vendors frequently provide the government with more information concerning their products or services than

they would make available in ordinary trade.” See also Treas. Reg. § 601.702(g) (requiring notice of a request to the contractor); Treas. Reg. § 301.9000-

3(b)(2), -4(f) (regarding disclosures in connection with testimony before Congress). Accordingly, the National Taxpayer Advocate has the authority to review

the agency record upon providing appropriate assurances that we will not disclose any confidential information to the public.

9

GAO, GAO-11-481, 2011 Tax Filing: IRS Dealt with Challenges to Date but Needs Additional Authority to Verify Compliance 4 (Mar. 31, 2011). For a com-

prehensive discussion of prepaid card features, see Michelle Jun, Consumers Union, Prepaid Cards: Second-Tier Bank Account Substitutes (Sept. 2010).

Section One — Most Serious Problems

336

A Proactive Approach to Developing a Government-Issued Debit Card

to Receive Tax Refunds Will Benefit Unbanked Taxpayers

Legislative

Recommendations

Most Serious

Problems

Most Litigated

Issues

Case Advocacy Appendices

underbanked. The following table sets forth the income levels and average refund

amounts for these populations:

TABLE 1.19.1, Financial Status of the Unbanked and Underbanked Population

10

Household

Annual Income Level

Percentage of

Unbanked Population

Percentage of

Underbanked

Population

Average/Median

Refund in Income

Range

Total Number of Individual

Income Tax Returns in this

Income Level

Less than $15,000 55.8 % 17.5% $1,247 / $539 35.3 million

$15,000 to $30,000 26.1% 23.3% $2,454 / $1,430 30.2 million

More than $30,000 18.1% 59.2% $2,066 / $1,730 76 million

Improve Financial Literacy. A debit card program would improve the financial

literacy of taxpayers by providing the unbanked with access to an ongoing financial

account to obtain banking services, i.e., a steppingstone to becoming comfortable with

financial institutions and banking activity.

Fraud Protection. Debit cards can protect taxpayers whose cards are lost or stolen.

Commercial debit cards have recently been used to commit fraud.

11

Identity thieves

obtain Social Security numbers, file returns using the real taxpayer’s name and a ficti-

tious income, buy a commercial debit card, and ask the IRS to issue the refund to that

card. Law enforcement officials have suggested the IRS prohibit use of debit cards to

curtail the fraudulent activity. However, the government can work with the private sec-

tor, which has experience in managing debit and credit card fraud, to design a program

with the least risk.

The government benefits from a debit card program in the following ways:

Reduced costs. When more taxpayers receive refunds electronically, the government

reduces check printing and mailing expenses. However, a debit card program is not

without costs, especially for distribution of the cards. The key to a cost-effective pro-

gram is to encourage taxpayers to use the card over several years and eventually switch

to direct deposit.

Control Over Card Features and Marketing. By sponsoring its own card, the govern-

ment will be able to use its purchasing power to exercise some level of control over the

features of the card, the fees, and the messages to taxpayers.

10

The unbanked and underbanked data reflect 2011 household income data. FDIC, 2011 FDIC National Survey of Unbanked and Underbanked Households

23 (Sept. 2012). However, the average and median refund data reflect tax year 2010 data and correlates to total positive income (TPI). IRS Compliance

Data Warehouse, Tax Year 2010, Individual Returns Transaction File.

11

Scott Zamost and Randi Kaye, IRS Policies Help Fuel Tax Refund Fraud, Officials Say, CNN.com (Mar. 20, 2012).

Taxpayer Advocate Service — 2012 Annual Report to Congress — Volume One

337

MSP #19

A Proactive Approach to Developing a Government-Issued Debit Card

to Receive Tax Refunds Will Benefit Unbanked Taxpayers

Legislative

Recommendations

Most Serious

Problems

Most Litigated

Issues

Case AdvocacyAppendices

Most Serious Problem

Legislative

Recommendations

Most Serious

Problems

Most Litigated

Issues

Case AdvocacyAppendices

The National Taxpayer Advocate, the Federal Government, and the Urban Institute

Have Recognized the Benefits of a Debit Card Program.

The National Taxpayer Advocate and Treasury agree that a debit card program would

benefit both unbanked taxpayers and tax administration. In the 2008 and 2011 Annual

Reports to Congress, the National Taxpayer Advocate recommended that Treasury enable

unbanked taxpayers to receive refunds on stored value cards (SVCs) or debit cards.

12

The federal government already directly participates in the debit card market outside the

tax system, as more than 90 government-funded programs use some form of prepaid card

to deliver benefits. In 2008, Treasury launched the Direct Express Debit MasterCard, used

by over 2.5 million individuals to receive federal benefits (such as Social Security pay-

ments), pay bills, make purchases, and access cash.

13

In addition, almost all VITA and TCE

sites offer at least one commercial debit card product.

Citing the benefits of debit cards for both the government and taxpayers, Treasury began

pilot-testing a tax refund debit card program in the 2011 filing season. The Tax Time

Account Direct Mail Pilot offered refunds on debit cards to more than 800,000 low income

taxpayers, who had less than $35,000 per year in household income and were believed to

have lived in unbanked or underbanked households.

14

Taxpayers received a reloadable

Visa-branded debit card called MyAccountCard from a bank selected by Treasury, and were

randomly assigned one of eight offers to test how they would respond to different offers.

15

The pilot was not designed to measure overall take-up but to test the effects of different

aspects of the card offers on take-up. Therefore, the recipients were divided into eight

treatment groups based on the type of offer they received. The offers varied in the follow-

ing ways:

Monthly fee (either no fee or $4.95);

Whether the card had access to a savings account:

The promotion message (either convenience or safety); and

The timing of the mailing (late January or mid-February).

16

12

National Taxpayer Advocate 2008 Annual Report to Congress 423-26 (Legislative Recommendation: Refund Delivery Options); National Taxpayer Advocate

2011 Annual Report to Congress 404-19 (Most Serious Problem: After Refund Anticipation Loans: Taxpayers Require Improved Education About Refund

Delivery Options and the Availability of a Government-Sponsored Debit Card).

13

See http://www.fms.treas.gov/directexpresscard/index.html (last visited Sept. 9, 2012); Caroline Ratcliffe, Signe-Mary McKernan, Urban Institute, Tax Time

Account Direct Mail Pilot Evaluation 3 (Sept. 2012).

14

The pilot sent offers to 808,099 taxpayers believed to be unbanked or underbanked. The household likelihood of being unbanked or underbanked was

a variable constructed by Experian Marketing Solutions Inc. using commercially available data and was based on a statistical model that produced an

underbanked score. Id. at ES-2, 3.

15

Treasury selected Bonneville Bank for the pilot and Bonneville selected Green Dot to provide card-processing services for the debit card that could be used

at any point-of-sale terminal that accepts VISA cards worldwide. Caroline Ratcliffe, Signe-Mary McKernan, Urban Institute, Tax Time Account Direct Mail

Pilot Evaluation ES-1 (Sept. 2012).

16

Id.

Section One — Most Serious Problems

338

A Proactive Approach to Developing a Government-Issued Debit Card

to Receive Tax Refunds Will Benefit Unbanked Taxpayers

Legislative

Recommendations

Most Serious

Problems

Most Litigated

Issues

Case Advocacy Appendices

Treasury expected a low take-up rate, as with most direct mailing campaigns, and con-

tracted with the Urban Institute to evaluate the program.

17

Fewer than 2,000 of the over

800,000 people who were offered the cards applied for them, a take-up rate of approximate-

ly 0.3 percent.

18

As a result, Treasury ended the pilot after the 2011 filing season, citing low

participation.

The Urban Institute released a report evaluating the MyAccountCard Tax Time pilot in

September 2012. Notably, the report provided “[i]n sum, the federal government’s creation

of an option for tax filers to receive refunds directly onto a low-cost, account-linked card, as

tested in this pilot, is a concept with promise.”

19

It also offered the following findings:

20

The Urban Institute acknowledged the low take-up rate, but recognized that 0.3 percent

was within the 0.3 percent to 0.8 percent range for credit card direct-mail take-up rates

experienced in recent years.

The take-up rate was significantly higher for individuals who were most likely to live

in unbanked households. This group had a 0.8 percent take-up rate, nearly three times

the rate for the full pilot population and at the upper end of the expected rate for direct

mail card offers.

Only 16 percent of all cardholders and 48 percent of those with active accounts actu-

ally used the card as originally intended and direct deposited their refunds into the

card account.

Charging a $4.95 monthly maintenance fee decreased card applications by 42 percent.

In addition, the likelihood of using the card within six months of receiving it was 47

percent lower for recipients of cards with the fee.

Linking a savings account to the card had virtually no impact on take-up.

Product messaging (safety versus convenience) did not significantly influence behavior.

The timing of the card offer had a significant impact on the take-up rate. People who

were mailed the offer in mid-January were 85 percent more likely to apply than those

who received it in early February.

21

17

GAO, GAO-11-481, 2011 Tax Filing: IRS Dealt with Challenges to Date but Needs Additional Authority to Verify Compliance 17, 39 (Mar. 31, 2011); Hearing

on Financial Literacy: Empowering Americans to Make Informed Financial Decisions, Subcomm. on Oversight of Government Management, the Federal

Workforce, and the District of Columbia, S. Comm. on Homeland Security and Governmental Affairs, 112th Cong. (Apr. 12, 2011) (testimony of Acting Di-

rector Joshua Wright, Office of Financial Education and Financial Access, U.S. Department of the Treasury); Caroline Ratcliffe, Signe-Mary McKernan, Urban

Institute, Tax Time Account Direct Mail Pilot Evaluation ES-2 (Sept. 2012).

18

Eric Kroh, Treasury Won’t Renew Debit Card Refund Program in 2012, Spokesman Confirms, Tax Notes Today (Nov. 1, 2011); Financial Management Service

(FMS) Briefing to TAS by Phone (Sept. 5, 2012). Overall, 1,967 people (0.3 percent of the offer recipients) applied for the prepaid card, of which 1,933

individuals (98.3 percent of applicants) were issued the card. Caroline Ratcliffe, Signe-Mary McKernan, Urban Institute, Tax Time Account Direct Mail Pilot

Evaluation ES-3 (Sept. 2012).

19

Caroline Ratcliffe, Signe-Mary McKernan, Urban Institute, Tax Time Account Direct Mail Pilot Evaluation ES-5 (Sept. 2012).

20

Id. at ES-3-4, 4, 7, 14, 15, 18, 19, 28.

21

The two-tiered mailing was not originally planned but was conducted consistently across the eight treatment groups. Caroline Ratcliffe, Signe-Mary McKer-

nan, Urban Institute, Tax Time Account Direct Mail Pilot Evaluation 7 (Sept. 2012).

Taxpayer Advocate Service — 2012 Annual Report to Congress — Volume One

339

MSP #19

A Proactive Approach to Developing a Government-Issued Debit Card

to Receive Tax Refunds Will Benefit Unbanked Taxpayers

Legislative

Recommendations

Most Serious

Problems

Most Litigated

Issues

Case AdvocacyAppendices

Most Serious Problem

Legislative

Recommendations

Most Serious

Problems

Most Litigated

Issues

Case AdvocacyAppendices

Based on the findings of the pilot study, the Urban Institute suggested the following steps

to increase take-up rates in any future debit card program:

22

Offer an account with a monthly fee as low as possible, even at the expense of other

card features such as savings account linkage.

Distribute and make the cards available before the tax-filing season begins.

Offer the card directly in the filing and refund process to reduce barriers to application.

Remove the multi-step application and deposit process for simplicity.

Enable taxpayers to use the card to pay tax preparation fees.

Publicize the card broadly and before the tax season to increase familiarity with the

product. A comprehensive informational “surround sound” campaign would use

earned and paid media and community partners to make the public aware of the card’s

existence and the application process. The 2011 pilot did not include a comprehensive

marketing campaign because the administrators did not want to contaminate compari-

sons across the different categories of offer recipients.

Accept individual taxpayer identification numbers (ITINs) to increase the take-up rate.

The pilot only accepted applications with Social Security numbers.

Notwithstanding Termination of the 2011 Treasury Debit Card Pilot, a Nationwide

Program Could Succeed With Improved Marketing and Distribution.

We are disappointed that Treasury discontinued the debit card pilot after just one filing

season. We realize that participation was lower than expected, perhaps because direct mail-

ing did not work well with this population. However, the IRS and Treasury may be able to

reach more unbanked and underbanked taxpayers by evaluating the pilot and the Urban

Institute report to develop a more successful distribution and marketing strategy.

The IRS’s response to the related Most Serious Problem in the National Taxpayer

Advocate’s 2011 Annual Report to Congress merely stated:

Due to the low participation rate, Treasury made a decision to terminate the 2011

Treasury-sponsored debit card pilot for tax refunds and will not offer the cards

during the 2012 filing season. If Treasury considers sponsoring a debit card for tax

refunds in future tax years, the IRS would work with it to explore the feasibility

and options.

23

The National Taxpayer Advocate believes the IRS’s response displays remarkable pas-

sivity in the face of the need of unbanked and underbanked taxpayers. The IRS should

engage with Treasury and the Taxpayer Advocate Service to take a more proactive role in

22

Caroline Ratcliffe, Signe-Mary McKernan, Urban Institute, Tax Time Account Direct Mail Pilot Evaluation ES-3 to -5, 4, 5 (Sept. 2012).

23

National Taxpayer Advocate 2011 Annual Report to Congress 416.

Section One — Most Serious Problems

340

A Proactive Approach to Developing a Government-Issued Debit Card

to Receive Tax Refunds Will Benefit Unbanked Taxpayers

Legislative

Recommendations

Most Serious

Problems

Most Litigated

Issues

Case Advocacy Appendices

developing a future project based on the experience and lessons learned from the 2011

pilot, with particular focus on the findings and conclusions of the Urban Institute.

As mentioned in the Urban Institute report, the distribution channels and application

process used in the 2011 pilot proved problematic. The direct-mail approach may not be

particularly useful, especially given the transient nature of this population. At the very

least, potential users should be offered the cards well in advance of the filing season.

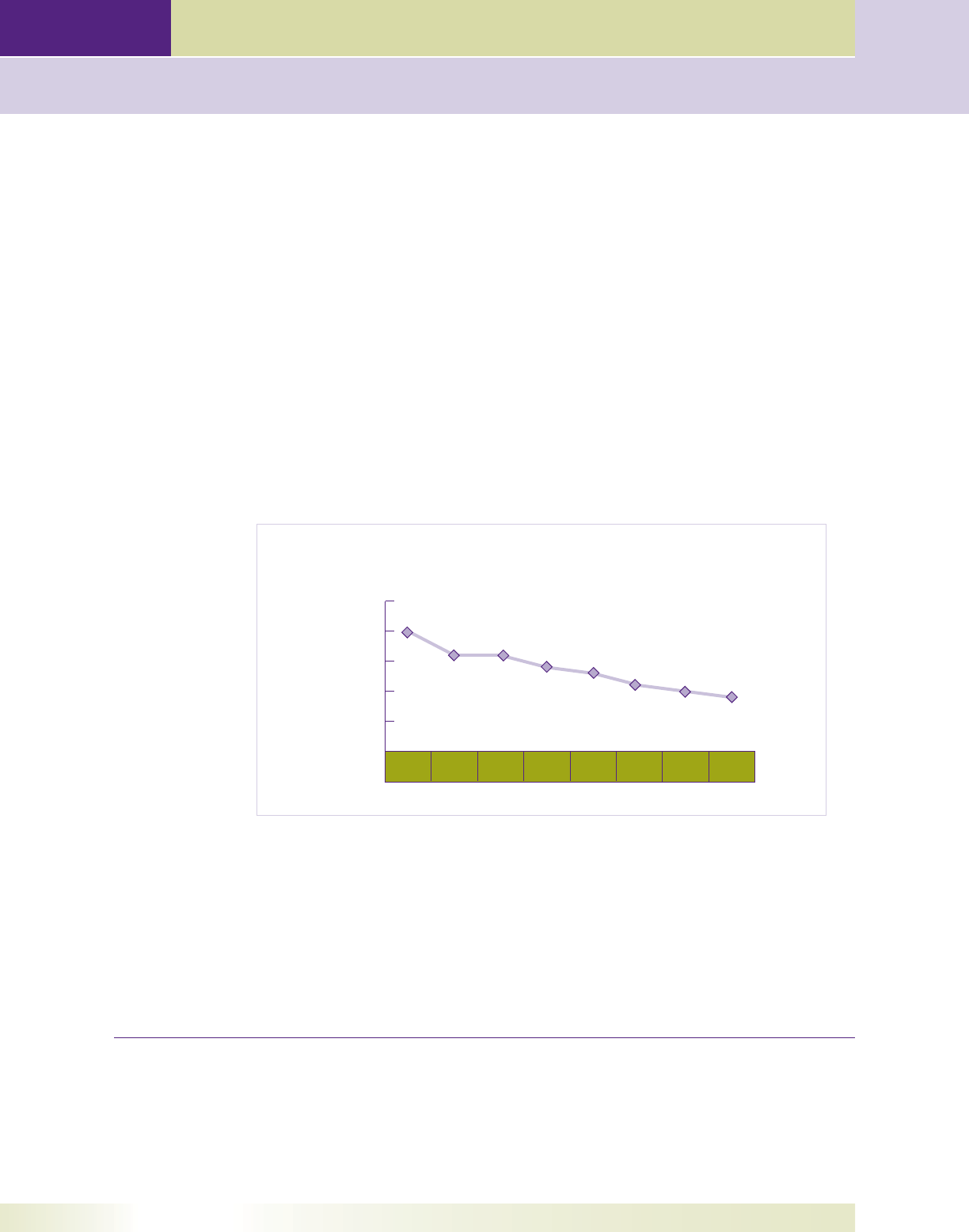

To illustrate the high mobility of this population, the following chart sets forth the percent-

age of individuals with income who moved in 2011, by income category. It illustrates that

those at lower income levels generally have a higher degree of mobility than others with

higher income.

24

FIGURE 1.19.2, Individuals Who Moved by Income Category

PERCENT

Geographic Mobility: Percent of U.S. Individuals Who Moved by Income Level

(Compared 2011 to 2010)

0%

5%

10%

15%

20%

25%

$75,000+$65,000-

$74,999

$50,000-

$64,999

$35,000-

$49,999

$25,000-

$34,999

$15,000-

$24,999

$10,000-

$14,999

$1-$9,999

or loss

20%

16%

13%

11%

10%

16%

14%

9%

Further, as discussed in the Urban Institute report, taxpayers may be more willing to

participate if the application process was streamlined and, ideally, incorporated into the tax

filing process by including it on IRS forms.

Another potential distribution channel would be to make the card application process avail-

able through the U.S. Post Office, similar to passport applications, or through banking insti-

tutions.

25

For example, taxpayers could indicate on their returns that they would like their

24

U.S. Census Bureau, 2011 American Community Survey 1-Year Estimates, B07010: Geographical Mobility in the Past Year by Individual Income in the Past

12 Months (In 2011) (the percentage numbers reflect the portion of the total population of individuals with income who moved, or who stayed in the same

location, as the case may be).

25

In Australia, individuals can obtain a Load&Go card at the post office. This product is a reloadable Visa prepaid debit card. For more information, see

http://auspost.com.au/personal/what-is-loadandgo-card.html (last visited Sept. 8, 2012). In the United Kingdom, taxpayers can receive the child benefit,

tax credits, and Guardian’s Allowance on the Post Office card account, which is administered at local post offices. HM Revenue & Customs, How Child

Benefit, tax credits and Guardian Allowance are paid, http://www.hmrc.gov.uk/childbenefit/payments-entitlements/payments/how-paid.htm (Last visited

Sept. 9, 2012).

Taxpayer Advocate Service — 2012 Annual Report to Congress — Volume One

341

MSP #19

A Proactive Approach to Developing a Government-Issued Debit Card

to Receive Tax Refunds Will Benefit Unbanked Taxpayers

Legislative

Recommendations

Most Serious

Problems

Most Litigated

Issues

Case AdvocacyAppendices

Most Serious Problem

Legislative

Recommendations

Most Serious

Problems

Most Litigated

Issues

Case AdvocacyAppendices

refunds delivered on the government debit card. Once the IRS accepts and processes the

taxpayer’s return, the taxpayer could go to any banking institution and receive the loaded

debit card, upon proof of identity. (This approach significantly addresses law enforcement

concerns about identity theft.) No matter which distribution channel the IRS chooses, the

program must include a comprehensive public awareness campaign to spread the word to

the target taxpayers and the preparers serving them.

In addition, our office discussed the 2011 pilot and the potential for a future debit card pro-

gram with officials of the Financial Management Service (FMS). Based on these conversa-

tions, we have learned several interesting facts:

26

The Direct Mailing List Used in the 2011 Pilot May Not Have Been Optimal. When

designing the project, the team planned to target unbanked and underbanked taxpay-

ers, and initially attempted to obtain a list of Earned Income Tax Credit (EITC) recipi-

ents as the target audience. However, information-sharing issues prevented the IRS

from providing this tax data.

27

Therefore, the team obtained the necessary list from an

outside party. The quality of this list may not have been optimal for the project, which

may explain why so few responded and so many mailings were returned as undeliv-

erable.

28

Further, the third-party data could not distinguish between those with Social

Security numbers, required for the pilot, and those without.

29

Application During the Tax Filing Process. As mentioned in the Urban Institute

report, an effective application process and distribution channel for the debit cards

are imperative. To make the take-up rate high enough to make the project successful

and financially viable, the IRS may need to give taxpayers a way to apply for the card

during the tax filing process. This would require changes to the Form 1040 series to

allow taxpayers to opt in to the program and consent to share information with the

financial institutions issuing the cards. The government can either collaborate with

one financial institution for simplicity or provide the taxpayer with a choice of several

institutions with which the government has negotiated appropriate terms. Certain

financial institutions may have a larger presence in different geographic regions. The

IRS would need to work proactively with Treasury to determine the most administra-

tively feasible and effective approach.

Current Technology Cannot Deliver All Government Benefits Through One

Government Card. It is not possible with current technology to distribute federal

payments such as Social Security Administration (SSA), Railroad Retirement (RR), and

Veteran’s Affairs (VA) benefits on the same card as tax refunds. Certain federal benefit

payments are exempt from garnishment orders received and executed by financial

26

FMS briefing to TAS by phone (Sept. 5, 2012).

27

IRC § 6103.

28

The list was not optimal for several reasons, including: (1) The list could not exclude individuals without Social Security numbers, a requirement for pilot

participation; (2) Whether an individual was unbanked or underbanked was predicted based on multiple variables from several sources. Caroline Ratcliffe,

Signe-Mary McKernan, Urban Institute, Tax Time Account Direct Mail Pilot Evaluation 5, 9 (Sept. 2012).

29

The high rate of undeliverable mail may also be explained by the transient nature of the unbanked and underbanked population.

Section One — Most Serious Problems

342

A Proactive Approach to Developing a Government-Issued Debit Card

to Receive Tax Refunds Will Benefit Unbanked Taxpayers

Legislative

Recommendations

Most Serious

Problems

Most Litigated

Issues

Case Advocacy Appendices

institutions.

30

It is our understanding that debit cards are linked to one account with

no ability to place the protected and unprotected funds in separate “buckets.” If a fi-

nancial institution receives a garnishment order, it has no way to identify which funds

in the debit card account are protected federal benefits once the funds are commingled

with other unprotected funds, such as tax refunds. Thus, it is currently impossible to

consolidate all government-sponsored debit card programs into one. However, future

technology is expected to allow taxpayers to designate at the point of sale the “bucket”

from which the funds should originate, which would isolate the funds derived from

protected benefits from the unprotected funds.

31

Source of Funds is Limited. During the 2011 pilot, it became apparent that financial

institutions resist allowing the cards to load payments other than government pay-

ments due to the risk of fraud. Any additional risk to the bank increases the potential

fees imposed on the cardholders. For example, unbanked taxpayers would benefit

from receiving tax refunds and payroll funds on a single card. However, if a bad or sto-

len check is deposited into an account and the funds are made immediately available

but the check does not subsequently clear, the bank loses the money.

32

To compensate

for this additional risk exposure, the bank may charge fees at a level unacceptably high

for a government-sponsored card. The government could attempt to alleviate this risk

by accumulating a list of trusted partner payroll providers and large employers, but

this approach would raise the issue of fairness if it appears the government is selecting

certain employers over others. This approval process may also be cost-prohibitive for

the government.

Many unbanked and underbanked taxpayers already own a debit card. It is our under-

standing that the IRS cannot distinguish between a traditional bank account and an

account linked to a debit card when it releases a refund.

33

After analyzing any potential

fraud or security risks, the IRS and Treasury can collaborate with private industry to

inform taxpayers that they already have access to an electronic refund delivery option

and can avoid incurring unnecessary fees to access the refund quickly. This endeavor will

require the participation of the private sector because not all cards will allow deposits from

multiple sources and the account numbers on the faces of the cards are not the same as the

numbers required for tax filing. Taxpayers would need to check with their financial institu-

tions about the details specific to their own cards.

34

30

31 C.F.R. § 212.6; Department of Treasury, FMS, Guidelines for Garnishment of Accounts Containing Federal Benefit Payments (March 2011). In 2009, the

National Taxpayer Advocate recommended that Congress amend IRC § 6402 to prohibit the Secretary from offsetting a taxpayer’s refund by more than 15

percent of the portion attributable to the earned income tax credit (EITC). National Taxpayer Advocate 2009 Annual Report to Congress 365-70.

31

FMS briefing to TAS by phone (Sept. 5, 2012).

32

The same issue arises with check-kiting schemes. FMS briefing to TAS by phone (Sept. 5, 2012); FMS briefing to TAS (Sept. 27, 2012).

33

FMS briefing to TAS by phone (Sept. 5, 2012); IRM 21.4.1.4.7 (July 12, 2012).

34

FMS briefing to TAS by phone (Sept. 5, 2012).

Taxpayer Advocate Service — 2012 Annual Report to Congress — Volume One

343

MSP #19

A Proactive Approach to Developing a Government-Issued Debit Card

to Receive Tax Refunds Will Benefit Unbanked Taxpayers

Legislative

Recommendations

Most Serious

Problems

Most Litigated

Issues

Case AdvocacyAppendices

Most Serious Problem

Legislative

Recommendations

Most Serious

Problems

Most Litigated

Issues

Case AdvocacyAppendices

An Aggressive Response is Necessary to Address the Incorporation of a Western

Union Product into TaxWise.

The IRS claims it does not endorse any particular debit card product. However, the

National Taxpayer Advocate believes the incorporation of Western Union’s MoneyWise

prepaid card in the TaxWise software, which the IRS provides to VITA and TCE sites free

of charge, creates an unfair advantage and an indirect endorsement by the IRS. When the

National Taxpayer Advocate raised this issue in the 2011 Annual Report, the IRS responded

that the debit card feature was not part of the software when the IRS entered into the CCH

contract.

35

In return, we urged the IRS to eliminate all references to the commercial prod-

uct in TaxWise software and marketing materials.

36

However, it is our understanding that

the product is still incorporated into TaxWise.

37

In fact, the IRS receives a monthly activity

report from TaxWise including data on the number of cards issued. As of September 1,

2012, over 4,000 taxpayers using VITA services purchased the product.

38

We believe the IRS is not acting aggressively enough to protect taxpayers in this in-

stance.

39

If the product was added to the software without IRS approval, the IRS likely

has the authority under the existing contract to demand that it be eliminated immediately.

Conversely, if the product was added with IRS approval, it is an improper endorsement and

gives an unfair edge to a relatively high-fee commercial option. The IRS should review the

terms of the contract to pursue the immediate elimination of all references by TaxWise to

the debit card product in software packages and marketing materials distributed to volun-

teer sites. Once the product is removed, it can be offered externally with other debit card

products.

Further, when the IRS renegotiates the contract with CCH for VITA/TCE electronic

preparation and transmission of returns, we urge the IRS to address debit cards as well as

other commercial refund products. The IRS has the authority to review the terms of all

commercial products offered through the software, and should require the vendor to seek

IRS approval before marketing any such product on software for volunteer organizations.

35

IRS response to Most Serious Problem, National Taxpayer Advocate 2011 Annual Report to Congress 410, 415.

36

National Taxpayer Advocate 2011 Annual Report to Congress 417.

37

See Western Union MoneyWise Prepaid MasterCard Overview, http://cchsfs-taxwise.custhelp.com/app/answers/detail/a_id/382/~/western-union-

moneywise-prepaid-mastercard-overview (last visited Sept. 9, 2012); TaxWise Desktop, Applying for the MoneyWise Card in a Return, available at http://

tax-coalition.org/program-tools/financial-services/asset-building/asset-building-products/debit-cards/western-union-moneywise-card/taxwise-desktop-

moneywise (last visited Sept. 9, 2012); GAO, GAO-11-481, 2011 Tax Filing: IRS Dealt with Challenges to Date but Needs Additional Authority to Verify

Compliance 38 (Mar. 2011).

38

According to IRS monthly reports, 4,047 taxpayers purchased the product. IRS response to TAS information request (Oct. 4, 2012).

39

For a list of the various fees charged by the debit cards offered at VITA/TCE sites during the 2011 filing season, see GAO, GAO-11-481, 2011 Tax Filing: IRS

Dealt with Challenges to Date but Needs Additional Authority to Verify Compliance 38 (Mar. 2011). For example, all of the programs had such favorable

terms as free activation and monthly maintenance on all programs. However, the Western Union program seemed to have the highest transactional fees,

with $1.95 per ATM withdrawal fees, $4.95 cash reload fees, and no relationship building with any financial institution.

Section One — Most Serious Problems

344

A Proactive Approach to Developing a Government-Issued Debit Card

to Receive Tax Refunds Will Benefit Unbanked Taxpayers

Legislative

Recommendations

Most Serious

Problems

Most Litigated

Issues

Case Advocacy Appendices

Moreover, the IRS should make it clear to the VITA/TCE partners and their customers that

it does not endorse any commercial refund products.

40

CONCLUSION

The IRS and Treasury need to take a more proactive approach to providing a free electronic

refund delivery option to unbanked and underbanked taxpayers. Treasury took an impor-

tant first step when it conducted the 2011 debit card pilot. While Treasury unfortunately

terminated the pilot after only one filing season, the pilot findings and the evaluation by

the Urban Institute provide valuable information for designing a nationwide program.

In addition, we remain concerned that TaxWise, the tax preparation software provided free

of charge by the IRS to VITA and TCE organizations, continues to incorporate the Western

Union MoneyWise prepaid card into program. The IRS has no control over the terms

associated with this product, yet appears to endorse the product by allowing the software to

offer it.

IRS COMMENTS

The IRS provides several options to taxpayers for receiving their federal income tax re-

funds. The IRS delivers extensive communications and outreach during each filing season

on the refund delivery options and encourages taxpayers to consider electronic options

such as direct deposit into their checking or savings account since it gives them access to

their refund faster than a paper check. It also avoids the possibility that a check could be

lost or stolen or returned to IRS as undeliverable. Taxpayers may also split their refunds

with direct deposits into two or three of their accounts and consider receiving their refund

electronically on a commercially-provided debit card.

In this report, the National Taxpayer Advocate suggests that the IRS make a government-

sponsored tax refund debit card available nationwide. In 2011, Treasury launched this

option through a pilot program called MyAccountCard (MAC) offering a selected group

of low- to mid-income taxpayers the opportunity to receive their refunds in the form of a

prepaid debit card. Only taxpayers who received a letter from Treasury were eligible to ap-

ply for the program. Treasury offered variations of MAC through three different financial

institutions to evaluate which product features, fee structures, and marketing messages

generated the greatest positive taxpayer response. Treasury made a decision to terminate

the debit card pilot for refunds and did not offer it for the 2012 filing season. The IRS will

work with the Treasury Department if it decides to explore a similar option in the future.

40

In a 2011, the IRS Wage & Investment Research organization conducted eight focus groups in four geographically dispersed cities to obtain taxpayers’ input

on their experiences with VITA. The report noted a “[g]eneral disinterest in investing in savings bonds and receiving pre-paid debit cards.” This finding is

worthy of further investigation. W&I Research & Analysis, 2011 Taxpayer Experience Focus Groups, Project Briefing for Stakeholder Partnerships, Education

& Communication (SPEC), Slide 12, Project # 4-10-01-S-058 (July 2011).

Taxpayer Advocate Service — 2012 Annual Report to Congress — Volume One

345

MSP #19

A Proactive Approach to Developing a Government-Issued Debit Card

to Receive Tax Refunds Will Benefit Unbanked Taxpayers

Legislative

Recommendations

Most Serious

Problems

Most Litigated

Issues

Case AdvocacyAppendices

Most Serious Problem

Legislative

Recommendations

Most Serious

Problems

Most Litigated

Issues

Case AdvocacyAppendices

VITA/TCE partners can select a software program that may offer a commercial debit card,

as long as that software meets the IRS guidelines for tax preparation and return submis-

sion. These sites are not required to report the offering of debit cards, and the IRS does

not generally track debit card offerings. However, the IRS does have information on debit

cards offered last year through the software contract with CCH TaxWise, a commercial-

off-the-shelf tax preparation and transmission product. As of September 1, 2012, eight

percent of VITA/TCE sites (1,076/13,143 sites) offered Western Union debit cards in lieu of

paper checks. These sites issued a total of 4,047 debit cards, which represents over one-

tenth of one percent (.12 percent) of all returns prepared through the VITA/TCE program

(4,047/3,267,997).

In December 2009, the IRS awarded a new software contract to CCH for the purchase of

TaxWise software. The debit card feature was incorporated into this software subsequent

to the award of the contract. The National Taxpayer Advocate has requested that the IRS

immediately require the CCH to remove all references to the Western Union debit card

product from the standard TaxWise software the IRS provides to VITA/TCE sites. In

response to concerns raised by the National Taxpayer Advocate, the IRS has requested that

CCH block access to the debit card feature in the software in the TY 2012 filing season. As

noted in our response to the MSP on Return Filing Options, the new 2014 contract will also

include a prohibition on offering a debit card product in software purchased by the IRS.

The National Taxpayer Advocate recommends that the IRS undertake an aggressive public

awareness campaign to educate taxpayers about the reduced return processing time as well

as its impact on refund turnaround times for government-sponsored refund options. While

the IRS can predict a general refund delivery timeframe, it cannot predict which taxpay-

ers will fall outside that timeframe or why. We have found it most helpful for taxpayers

to communicate realistic refund delivery times. Analysis of call center traffic, focus group

results, feedback from the tax preparer and tax software industries, combined with IRS

experience, support the conclusion that taxpayers will count on the best case scenario for

refund issuance if IRS sets expectations for consumers using a range (ten to 21 days, for

example). Despite caveats and cautious language, taxpayers who want their refunds faster

consistently count on the nearest date and call in frustration when their expectations are

not met. Not only is this not in the taxpayer’s best interest, but it also puts unnecessary

pressure on the IRS and tax industry customer service operations, diverting services from

other taxpayer needs.

In 2013, we will implement consumer messaging, setting a general expectation for refunds

in less than 21 days, and directing taxpayers to the Where’s My Refund tool where they

will see information about their own personal refund instead of a generic, estimated date.

This year, taxpayers will be able to start checking on the status of their return within 24

hours (instead of 72) after the IRS has received an e-filed return. Also in 2013, Where’s My

Refund will include a tracker that displays progress through the following three stages: (1)

Return Received, (2) Refund Approved and (3) Refund Sent.

Section One — Most Serious Problems

346

A Proactive Approach to Developing a Government-Issued Debit Card

to Receive Tax Refunds Will Benefit Unbanked Taxpayers

MSP #19

Legislative

Recommendations

Most Serious

Problems

Most Litigated

Issues

Case Advocacy Appendices

The IRS has considered stakeholder feedback and is committed to working together with

stakeholders to set expectations for refund communications and implement suggested

changes to Where’s My Refund. The IRS expects that each of those initiatives will improve

the taxpayer’s ability to understand their refund status. The IRS will also continue to

deliver messaging during filing season that the fastest way to get a tax refund is to use free

file or e-file to ensure an accurate tax return in addition to promoting the direct deposit

option. While the IRS works hard to issue refunds as quickly as possible, some tax returns

take longer to process than others for many reasons, including when a return has errors,

is incomplete or needs further review. We will ensure that taxpayers are informed as to

realistic expectations.

Taxpayer Advocate Service Comments

The IRS’s response regarding the development of a government-sponsored debit card

continues to display remarkable passivity in the face of the need of unbanked and under-

banked taxpayers to receive their refunds electronically free of charge. The IRS offered a

similar response to the related Most Serious Problem in the National Taxpayer Advocate’s

2011 Annual Report to Congress.

41

The National Taxpayer Advocate strongly believes it is

in the best interest of taxpayers and tax administration to make a government-sponsored

tax refund debit card available nationwide. Accordingly, the IRS should engage with

Treasury and the Taxpayer Advocate Service to proactively develop a future project, based

on the experience and lessons learned from the 2011 pilot, with particular focus on the

findings and conclusions of the Urban Institute.

The National Taxpayer Advocate commends the IRS for taking a firm stance against the in-

corporation of the Western Union debit card in TaxWise software for VITA and TCE sites.

By requesting that CCH block access to this feature during the coming filing season, the

IRS has sent a strong message that it will not tolerate the inclusion of commercial refund

products in software provided to volunteers without prior IRS approval. In addition, the

planned prohibition on such products in the 2014 contract with CCH will resolve the issue

in the future.

Finally, we continue to believe that taxpayers can make more informed decisions about

whether to buy commercial refund delivery products if an aggressive IRS public awareness

campaign provides information on refund turnaround times for various delivery methods

in the previous filing season. We understand that the IRS has competing concerns in this

area because any deviation from the times provided in such communications will drive

taxpayers to call the IRS and drain already scarce resources. However, carefully drafted

messages could set forth the expected range for the current year as well as actual times

41

See National Taxpayer Advocate 2011 Annual Report to Congress 414-16.

Taxpayer Advocate Service — 2012 Annual Report to Congress — Volume One

347

A Proactive Approach to Developing a Government-Issued Debit Card

to Receive Tax Refunds Will Benefit Unbanked Taxpayers

MSP #19

Legislative

Recommendations

Most Serious

Problems

Most Litigated

Issues

Case AdvocacyAppendices

Most Serious Problem

experienced in the past. If they know the actual average times from the last filing season,

taxpayers can form realistic expectations and have the information they need to determine

before they file their return which refund delivery method is best for them. Once they have

filed, taxpayers can use the enhanced “Where’s My Refund” application to keep informed

about the status of their refunds and receive more detailed information regarding the

estimated delivery date. The new, more tailored features of “Where’s My Refund” should

help to manage taxpayers’ expectations about refund delivery, and we commend the IRS for

these refinements.

Recommendations

The National Taxpayer Advocate recommends that the IRS take the following actions to

better serve unbanked and underbanked taxpayers:

1. In collaboration with the Department of Treasury and the Office of the Taxpayer

Advocate, establish a task force to evaluate the results of the Treasury debit card

pilot, with a particular focus on the Urban Institute report, to design a more effective

future nationwide program. The team should review the feasibility of incorporating

the application process into the tax-filing process as well as distribution of the cards

through the post office and financial institutions, and should confer with the private

and nonprofit sectors about security and consumer protection issues.

2. Provide the National Taxpayer Advocate with a complete copy of the agreement with

CCH concerning the TaxWise product used in the VITA program, and any forthcom-

ing Requests for Proposals pertaining to VITA software procurement, prior to public

announcement.

3. If the IRS wants the software it provides to VITA/TCE sites to include a debit card

product, explicitly state that requirement in its Request for Proposal and separately

negotiate terms for debit card services.

4. Undertake an aggressive public awareness campaign to educate taxpayers about the

reduced return processing time, as well as its impact on refund turnaround times,

for government-sponsored refund options. This campaign should inform taxpayers

about actual turnaround times during the previous filing season and advise taxpay-

ers to ask certain questions about card features before purchasing a commercial

refund product, such as a debit card.