PMBOK®Guide—FifthEdition

Pre‐ReleaseVersionOctober10,2012

©2012ProjectManagementInstitute.AllRightsReserved.

NotforDistributionorReproduction.

Figure 7-3. Plan Cost Management: Data Flow Diagram

The cost management processes and their associated tools and techniques are

documented in the cost management plan. The cost management plan is a component of the

project management plan.

7.1.1 Plan Cost Management: Inputs

7.1.1.1 Project Management Plan

Described in Section 4.2.3.1. The project management plan contains information used to

develop the cost management plan, which contains, but is not limited to:

Scope baseline. The scope baseline includes the project scope statement and WBS

detail for cost estimation and management.

Schedule baseline. The schedule baseline defines when the project costs will be

incurred.

Other information. Other cost-related scheduling, risk, and communications

decisions from the project management plan.

7.1.1.2 Project Charter

Described in Section 4.1.3.1. The project charter provides the summary budget from

which the detailed project costs are developed. The project charter also defines the project

approval requirements that will influence the management of the project costs.

7.1.1.3 Enterprise Environmental Factors

Described in Section 2.1.5. The enterprise environmental factors that influence the Plan

Cost Management process include, but are not limited to:

PMBOK®Guide—FifthEdition

Pre‐ReleaseVersionOctober10,2012

©2012ProjectManagementInstitute.AllRightsReserved.

NotforDistributionorReproduction.

Organizational culture and structure can all influence cost management;

Market conditions describe what products, services, and results are available in the

regional and global market;

Currency exchange rates for project costs sourced from more than one country;

Published commercial information such as resource cost rate information is often

available from commercial databases that track skills and human resource costs, and

provide standard costs for material and equipment. Published seller price lists are

another source of information; and

Project management information system, which provides alternative possibilities for

managing cost.

7.1.1.4 Organizational Process Assets

Described in Section 2.1.4. The organizational process assets that influence the Plan Cost

Management process include, but are not limited to:

Financial controls procedures (e.g., time reporting, required expenditure and

disbursement reviews, accounting codes, and standard contract provisions);

Historical information and lessons learned knowledge bases;

Financial databases; and

Existing formal and informal cost estimating and budgeting-related policies,

procedures, and guidelines.

7.1.2 Plan Cost Management: Tools and Techniques

7.1.2.1 Expert Judgment

Expert judgment, guided by historical information, provides valuable insight about the

environment and information from prior similar projects. Expert judgment can also suggest

whether to combine methods and how to reconcile differences between them.

Judgment based upon expertise in an application area, Knowledge Area, discipline,

industry, etc., as appropriate for the activity being performed should be used in developing the

cost management plan.

7.1.2.2 Analytical Techniques

Developing the cost management plan may involve choosing strategic options to fund the

project such as: self-funding, funding with equity, or funding with debt. The cost management

plan may also detail ways to finance project resources such as making, purchasing, renting, or

leasing. These decisions, like other financial decisions affecting the project, may affect project

schedule and/or risks.

Organizational policies and procedures may influence which financial techniques are

employed in these decisions. Techniques may include (but are not limited to): payback period,

return on investment, internal rate of return, discounted cash flow, and net present value.

7.1.2.3 Meetings

Project teams may hold planning meetings to develop the cost management plan.

Attendees at these meetings may include the project manager, the project sponsor, selected

PMBOK®Guide—FifthEdition

Pre‐ReleaseVersionOctober10,2012

©2012ProjectManagementInstitute.AllRightsReserved.

NotforDistributionorReproduction.

project team members, selected stakeholders, anyone with responsibility for project costs, and

others as needed.

7.1.3 Plan Cost Management: Outputs

7.1.3.1 Cost Management Plan

The cost management plan is a component of the project management plan and describes

how the project costs will be planned, structured, and controlled. The cost management processes

and their associated tools and techniques are documented in the cost management plan.

For example, the cost management plan can establish the following:

Units of measure. Each unit used in measurements (such as staff hours, staff days,

weeks for time measures; or meters, liters, tons, kilometers, or cubic yards for

quantity measures; or lump sum in currency form) is defined for each of the

resources.

Level of precision. The degree to which activity cost estimates will be rounded up or

down (e.g., US$100.49 to US$100, or US$995.59 to US$1,000), based on the scope

of the activities and magnitude of the project.

Level of accuracy. The acceptable range (e.g., ±10%) used in determining realistic

activity cost estimates is specified, and may include an amount for contingencies;

Organizational procedures links. The work breakdown structure (WBS) (Section

5.4) provides the framework for the cost management plan, allowing for consistency

with the estimates, budgets, and control of costs. The WBS component used for the

project cost accounting is called the control account. Each control account is assigned

a unique code or account number(s) that links directly to the performing

organization’s accounting system.

Control thresholds. Variance thresholds for monitoring cost performance may be

specified to indicate an agreed-upon amount of variation to be allowed before some

action needs to be taken. Thresholds are typically expressed as percentage deviations

from the baseline plan.

Rules of performance measurement. Earned value management (EVM) rules of

performance measurement are set. For example, the cost management plan may:

o Define the points in the WBS at which measurement of control accounts will be

performed;

o Establish the earned value measurement techniques (e.g., weighted milestones,

fixed-formula, percent complete, etc.) to be employed; and

o Specify tracking methodologies and the earned value management computation

equations for calculating projected estimate at completion (EAC) forecasts to

provide a validity check on the bottom-up EAC.

For more specific information regarding earned value management, refer to the Practice

Standard for Earned Value Management – Second Edition.

Reporting formats. The formats and frequency for the various cost reports are

defined.

Process descriptions. Descriptions of each of the other cost management processes

are documented.

PMBOK®Guide—FifthEdition

Pre‐ReleaseVersionOctober10,2012

©2012ProjectManagementInstitute.AllRightsReserved.

NotforDistributionorReproduction.

Additional details. Additional details about cost management activities include, but

are not limited to:

o Description of strategic funding choices,

o Procedure to account for fluctuations in currency exchange rates, and

o Procedure for project cost recording.

7.2 Estimate Costs

Estimate Costs is the process of developing an approximation of the monetary resources

needed to complete project activities. The key benefit of this process is that it determines the

amount of cost required to complete project work. The inputs, tools and techniques, and outputs

of this process are depicted in Figure 7-4. Figure 7-5 depicts the data flow diagram of the

process.

Figure 7-4. Estimate Costs: Inputs, Tools & Techniques, and Outputs

PMBOK®Guide—FifthEdition

Pre‐ReleaseVersionOctober10,2012

©2012ProjectManagementInstitute.AllRightsReserved.

NotforDistributionorReproduction.

Figure 7-5. Estimate Costs Data Flow Diagram

Cost estimates are a prediction that is based on the information known at a given point in

time. Cost estimates include the identification and consideration of costing alternatives to initiate

and complete the project. Cost trade-offs and risks should be considered, such as make versus

buy, buy versus lease, and the sharing of resources in order to achieve optimal costs for the

project.

Cost estimates are generally expressed in units of some currency (i.e., dollars, euros, yen,

etc.), although in some instances other units of measure, such as staff hours or staff days, are

used to facilitate comparisons by eliminating the effects of currency fluctuations.

Cost estimates should be reviewed and refined during the course of the project to reflect

additional detail as it becomes available and assumptions are tested. The accuracy of a project

estimate will increase as the project progresses through the project life cycle. For example, a

project in the initiation phase may have a rough order of magnitude (ROM) estimate in the range

of −25% to +75%. Later in the project, as more information is known, definitive estimates could

narrow the range of accuracy to -5% to +10%. In some organizations, there are guidelines for

when such refinements can be made and the degree of confidence or accuracy that is expected.

Sources of input information are derived from the outputs of processes in other

Knowledge Areas. Once received, all of this information will remain available as inputs to all of

the cost management processes.

PMBOK®Guide—FifthEdition

Pre‐ReleaseVersionOctober10,2012

©2012ProjectManagementInstitute.AllRightsReserved.

NotforDistributionorReproduction.

Costs are estimated for all resources that will be charged to the project. This includes, but

is not limited to, labor, materials, equipment, services, and facilities, as well as special categories

such as an inflation allowance, cost of financing, or contingency costs. A cost estimate is a

quantitative assessment of the likely costs for resources required to complete the activity. Cost

estimates may be presented at the activity level or in summary form.

7.2.1 Estimate Costs: Inputs

7.2.1.1 Cost Management Plan

Described in Section 7.1.3.1. The cost management plan defines how project costs will be

managed and controlled. It includes the method used and the level of accuracy required to

estimate activity cost.

7.2.1.2 Human Resource Management Plan

Described in Section 9.1.3.1. The human resource management plan provides project

staffing attributes, personnel rates, and related rewards/recognition, which are necessary

components for developing the project cost estimates.

7.2.1.3 Scope Baseline

The scope baseline is comprised of the following:

Project scope statement. The project scope statement (Section 5.3.3.1) provides the

product description, acceptance criteria, key deliverables, project boundaries,

assumptions, and constraints about the project. One basic assumption that needs to be

made when estimating project costs is whether the estimates will be limited to direct

project costs only or whether the estimates will also include indirect costs. Indirect

costs are those costs that cannot be directly traced to a specific project and therefore

will be accumulated and allocated equitably over multiple projects by some approved

and documented accounting procedure. One of the most common constraints for

many projects is a limited project budget. Examples of other constraints are required

delivery dates, available skilled resources, and organizational policies.

Work breakdown structure. The WBS (Section 5.4) provides the relationships

among all the components of the project and the project deliverables.

WBS dictionary. The WBS dictionary (Section 5.4.3.1) provides detailed

information about the deliverables and a description of the work for each component

in the WBS required to produce each deliverable.

Additional information that may be found in the scope baseline with contractual and legal

implications, such as health, safety, security, performance, environmental, insurance, intellectual

property rights, licenses, and permits. All of this information should be considered when

developing the cost estimates.

7.2.1.4 Project Schedule

Described in Section 6.6.3.2. The type and quantity of resources and the amount of time

which those resources are applied to complete the work of the project are major factors in

determining the project cost. Schedule activity resources and their respective durations are used

as key inputs to this process. Estimate Activity Resources (Section 6.4) involves determining the

availability of staff, the number of staff hours required, and quantities of material and equipment

needed to perform schedule activities. It is closely coordinated with cost estimating. Activity

PMBOK®Guide—FifthEdition

Pre‐ReleaseVersionOctober10,2012

©2012ProjectManagementInstitute.AllRightsReserved.

NotforDistributionorReproduction.

duration estimates (Section 6.5.3.1) will affect cost estimates on any project where the project

budget includes an allowance for the cost of financing (including interest charges) and where

resources are applied per unit of time for the duration of the activity. Activity duration estimates

can also affect cost estimates that have time-sensitive costs included in them, such as union labor

with regularly expiring collective bargaining agreements or materials with seasonal cost

variations.

7.2.1.5 Risk Register

Described in Section 11.2.3.1. The risk register should be reviewed to consider risk

response costs. Risks, which can be either threats or opportunities, typically have an impact on

both activity and overall project costs. As a general rule, when the project experiences a negative

risk event, the near-term cost of the project will usually increase, and there will sometimes be a

delay in the project schedule. In a similar way, the project team should be sensitive to potential

opportunities that can benefit the business either by directly reducing activity costs or by

accelerating the schedule.

7.2.1.6 Enterprise Environmental Factors

Described in Section 2.1.5. The enterprise environmental factors that influence the

Estimate Costs process include, but are not limited to:

Market conditions. These conditions describe what products, services, and results

are available in the market, from whom, and under what terms and conditions.

Regional and/or global supply and demand conditions greatly influence resource

costs.

Published commercial information. Resource cost rate information is often

available from commercial databases that track skills and human resource costs, and

provide standard costs for material and equipment. Published seller price lists are

another source of information.

7.2.1.7 Organizational Process Assets

Described in Section 2.1.4. The organizational process assets that influence the Estimate

Costs process include, but are not limited to:

Cost estimating policies,

Cost estimating templates,

Historical information, and

Lessons learned.

7.2.2 Estimate Costs: Tools and Techniques

7.2.2.1 Expert Judgment

Expert judgment, guided by historical information, provides valuable insight about the

environment and information from prior similar projects. Expert judgment can also be used to

determine whether to combine methods of estimating and how to reconcile differences between

them.

7.2.2.2 Analogous Estimating

Analogous cost estimating uses the values such as scope, cost, budget, and duration or

measures of scale such as size, weight, and complexity from a previous, similar project as the

PMBOK®Guide—FifthEdition

Pre‐ReleaseVersionOctober10,2012

©2012ProjectManagementInstitute.AllRightsReserved.

NotforDistributionorReproduction.

basis for estimating the same parameter or measurement for a current project. When estimating

costs, this technique relies on the actual cost of previous, similar projects as the basis for

estimating the cost of the current project. It is a gross value estimating approach, sometimes

adjusted for known differences in project complexity.

Analogous cost estimating is frequently used to estimate a value when there is a limited

amount of detailed information about the project, for example, in the early phases of a project.

Analogous cost estimating uses historical information and expert judgment.

Analogous cost estimating is generally less costly and less time consuming than other

techniques, but it is also generally less accurate. Analogous cost estimates can be applied to a

total project or to segments of a project, in conjunction with other estimating methods.

Analogous estimating is most reliable when the previous projects are similar in fact and not just

in appearance, and the project team members preparing the estimates have the needed expertise.

7.2.2.3 Parametric Estimating

Parametric estimating uses a statistical relationship between relevant historical data and

other variables (e.g., square footage in construction) to calculate a cost estimate for project work.

This technique can produce higher levels of accuracy depending upon the sophistication and

underlying data built into the model. Parametric cost estimates can be applied to a total project or

to segments of a project, in conjunction with other estimating methods.

7.2.2.4 Bottom-Up Estimating

Bottom-up estimating is a method of estimating a component of work. The cost of

individual work packages or activities is estimated to the greatest level of specified detail. The

detailed cost is then summarized or “rolled up” to higher levels for subsequent reporting and

tracking purposes. The cost and accuracy of bottom-up cost estimating are typically influenced

by the size and complexity of the individual activity or work package.

7.2.2.5 Three-Point Estimating

The accuracy of single-point activity cost estimates may be improved by considering

estimation uncertainty and risk and using three estimates to define an approximate range for an

activity’s cost:

Most likely (cM). The cost of the activity, based on realistic effort assessment for the

required work and any predicted expenses.

Optimistic (cO). The activity cost based on analysis of the best-case scenario for the

activity.

Pessimistic (cP). The activity cost based on analysis of the worst-case scenario for

the activity.

Depending on the assumed distribution of values within the range of the three estimates

the expected cost, cE, can be calculated using a formula. Two commonly used formulas are

triangular and beta distributions. The formulas are:

Triangular Distribution. cE

= (cO + cM + cP) / 3

Beta Distribution (from a traditional PERT analysis). cE = (cO + 4cM + cP) / 6

Cost estimates based on three points with an assumed distribution provide an expected

cost and clarify the range of uncertainty around the expected cost.

PMBOK®Guide—FifthEdition

Pre‐ReleaseVersionOctober10,2012

©2012ProjectManagementInstitute.AllRightsReserved.

NotforDistributionorReproduction.

7.2.2.6 Reserve Analysis

Cost estimates may include contingency reserves (sometimes called contingency

allowances) to account for cost uncertainty. Contingency reserves are the budget within the cost

baseline that is allocated for identified risks, which are accepted and for which contingent or

mitigating responses are developed. Contingency reserves are often viewed as the part of the

budget intended to address the “known-unknowns” that can affect a project. For example, rework

for some project deliverables could be anticipated, while the amount of this rework is unknown.

Contingency reserves may be estimated to account for this unknown amount of rework.

Contingency reserves can provide for a specific activity, for the whole project, or both. The

contingency reserve may be a percentage of the estimated cost, a fixed number, or may be

developed by using quantitative analysis methods.

As more precise information about the project becomes available, the contingency

reserve may be used, reduced, or eliminated. Contingency should be clearly identified in cost

documentation. Contingency reserves are part of the cost baseline and the overall funding

requirements for the project.

Estimates may also be produced for the amount of management reserve to be funded for

the project. Management reserves are an amount of the project budget withheld for management

control purposes and are reserved for unforeseen work that is within scope of the project.

Management reserves are intended to address the “unknown unknowns” that can affect a project.

The management reserve is not included in the cost baseline but is part of the overall project

budget and funding requirements. When an amount of management reserves is used to fund

unforeseen work, the amount of management reserve used is added to the cost baseline, thus

requiring an approved change to the cost baseline.

7.2.2.7 Cost of Quality (COQ)

Assumptions about costs of quality (Section 8.1.2.2) may be used to prepare the activity

cost estimate.

7.2.2.8 Project Management Software

Project management software applications, computerized spreadsheets, simulation, and

statistical tools are used to assist with cost estimating. Such tools can simplify the use of some

cost-estimating techniques and thereby facilitate rapid consideration of cost estimate alternatives.

7.2.2.9 Vendor Bid Analysis

Cost estimating methods may include analysis of what the project should cost, based on

the responsive bids from qualified vendors. When projects are awarded to a vendor under

competitive processes, additional cost estimating work may be required of the project team to

examine the price of individual deliverables and to derive a cost that supports the final total

project cost.

7.2.2.10 Group Decision-Making Techniques

Team-based approaches, such as brainstorming, the Delphi or nominal group techniques,

are useful for engaging team members to improve estimate accuracy and commitment to the

emerging estimates. By involving a structured group of people who are close to the technical

execution of work in the estimation process, additional information is gained and more accurate

estimates are obtained. Additionally, when people are involved in the estimation process, their

commitment towards meeting the resulting estimates increases.

PMBOK®Guide—FifthEdition

Pre‐ReleaseVersionOctober10,2012

©2012ProjectManagementInstitute.AllRightsReserved.

NotforDistributionorReproduction.

7.2.3 Estimate Costs: Outputs

7.2.3.1 Activity Cost Estimates

Activity cost estimates are quantitative assessments of the probable costs required to

complete project work. Cost estimates can be presented in summary form or in detail. Costs are

estimated for all resources that are applied to the activity cost estimate. This includes, but is not

limited to, direct labor, materials, equipment, services, facilities, information technology, and

special categories such as cost of financing (including interest charges),an inflation allowance,

exchange rates, or a cost contingency reserve. Indirect costs, if they are included in the project

estimate, can be included at the activity level or at higher levels.

7.2.3.2 Basis of Estimates

The amount and type of additional details supporting the cost estimate vary by

application area. Regardless of the level of detail, the supporting documentation should provide a

clear and complete understanding of how the cost estimate was derived.

Supporting detail for activity cost estimates may include:

Documentation of the basis of the estimate (i.e., how it was developed),

Documentation of all assumptions made,

Documentation of any known constraints,

Indication of the range of possible estimates (e.g., €10,000 (±10%) to indicate that the

item is expected to cost between a range of values), and

Indication of the confidence level of the final estimate.

7.2.3.3 Project Documents Updates

Project documents that may be updated include, but are not limited to, the risk register.

7.3 Determine Budget

Determine Budget is the process of aggregating the estimated costs of individual

activities or work packages to establish an authorized cost baseline. The key benefit of this

process is that it determines the cost baseline against which project performance can be

monitored and controlled. The inputs, tools and techniques, and outputs of this process are

depicted in Figure 7-6. Figure 7-7 depicts the data flow diagram of the process.

Figure 7-6. Determine Budget: Inputs, Tools & Techniques, and Outputs

PMBOK®Guide—FifthEdition

Pre‐ReleaseVersionOctober10,2012

©2012ProjectManagementInstitute.AllRightsReserved.

NotforDistributionorReproduction.

Figure 7-7. Determine Budget Data Flow Diagram

A project budget includes all the funds authorized to execute the project. The cost

baseline is the approved version of the time-phased project budget, but excludes management

reserves.

7.3.1 Determine Budget: Inputs

7.3.1.1 Cost Management Plan

Described in Section 7.1.3.1. The cost management plan describes how the project costs

will be managed and controlled.

7.3.1.2 Scope Baseline

Project scope statement. Formal limitations by period for the expenditure of project

funds can be mandated by the organization, by agreement (Section 12.2.3.2), or by

other entities such as government agencies. These funding constraints are reflected in

the project scope statement.

Work breakdown structure. The WBS (Section 5.4) provides the relationships

among all the project deliverables and their various components.

PMBOK®Guide—FifthEdition

Pre‐ReleaseVersionOctober10,2012

©2012ProjectManagementInstitute.AllRightsReserved.

NotforDistributionorReproduction.

WBS dictionary. The WBS dictionary (Section 5.4.3.1) and related detailed

statements of work provide an identification of the deliverables and a description of

the work in each WBS component required to produce each deliverable.

7.3.1.3 Activity Cost Estimates

Described in Section 7.2.3.1. Cost estimates for each activity within a work package are

aggregated to obtain a cost estimate for each work package.

7.3.1.4 Basis of Estimates

Described in Section 7.2.3.2. Supporting detail for cost estimates contained in the basis

for estimates should specify any basic assumptions dealing with the inclusion or exclusion of

indirect or other costs in the project budget.

7.3.1.5 Project Schedule

Described in Section 6.6.3.2. The project schedule includes planned start and finish dates

for the project’s activities, milestones, work packages, and control accounts. This information

can be used to aggregate costs to the calendar periods in which the costs are planned to be

incurred.

7.3.1.6 Resource Calendars

Described in Sections 9.2.3.2 and 12.2.3.3. Resource calendars provide information on

which resources are assigned to the project and when they are assigned. This information can be

used to indicate resource costs over the duration of the project.

7.3.1.7 Risk Register

Described in Section 11.2.3.1. The risk register should be reviewed to consider how to

aggregate the risk response costs. Updates to the risk register are included with project document

updates described in Section 11.5.3.2.

7.3.1.8 Agreements

Described in Section 12.2.3.2. Applicable agreement information and costs relating to

products, services, or results that have been or will be purchased are included when determining

the budget.

7.3.1.9 Organizational Process Assets

Described in Section 2.1.4. The organizational process assets that influence the

Determine Budget process include, but are not limited to:

Existing formal and informal cost budgeting-related policies, procedures, and

guidelines;

Cost budgeting tools; and

Reporting methods.

7.3.2 Determine Budget: Tools and Techniques

7.3.2.1 Cost Aggregation

Cost estimates are aggregated by work packages in accordance with the WBS. The work

package cost estimates are then aggregated for the higher component levels of the WBS (such as

control accounts) and ultimately for the entire project.

PMBOK®Guide—FifthEdition

Pre‐ReleaseVersionOctober10,2012

©2012ProjectManagementInstitute.AllRightsReserved.

NotforDistributionorReproduction.

7.3.2.2 Reserve Analysis

Budget reserve analysis can establish both the contingency reserves and the management

reserves for the project. Management and contingency reserves are addressed in more detail in

Section 7.2.2.6.

7.3.2.3 Expert Judgment

Expert judgment, guided by experience in an application area, Knowledge Area,

discipline, industry, or similar project, aids in determining the budget. Such expertise may be

provided by any group or person with specialized education, knowledge, skill, experience, or

training. Expert judgment is available from many sources, including, but not limited to:

Other units within the performing organization,

Consultants,

Stakeholders, including customers,

Professional and technical associations, and

Industry groups.

7.3.2.4 Historical Relationships

Any historical relationships that result in parametric estimates or analogous estimates

involve the use of project characteristics (parameters) to develop mathematical models to predict

total project costs. Such models may be simple (e.g., residential home construction is based on a

certain cost per square foot of space) or complex (e.g., one model of software development

costing uses multiple separate adjustment factors, each of which has numerous points within it).

Both the cost and accuracy of analogous and parametric models can vary widely. They

are most likely to be reliable when:

Historical information used to develop the model is accurate,

Parameters used in the model are readily quantifiable, and

Models are scalable, such that they work for large projects, small projects, and phases

of a project.

7.3.2.5 Funding Limit Reconciliation

The expenditure of funds should be reconciled with any funding limits on the

commitment of funds for the project. A variance between the funding limits and the planned

expenditures will sometimes necessitate the rescheduling of work to level out the rate of

expenditures. This is accomplished by placing imposed date constraints for work into the project

schedule.

7.3.3 Determine Budget: Outputs

7.3.3.1 Cost Baseline

The cost baseline is the approved version of the time-phased project budget, excluding

any management reserves, which can only be changed through formal change control procedures

and is used as a basis for comparison to actual results. It is developed as a summation of the

approved budgets for the different schedule activities.

Figure 7-8 illustrates the various components of the project budget and cost baseline.

Activity cost estimates for the various project activities along with any contingency reserves

PMBOK®Guide—FifthEdition

Pre‐ReleaseVersionOctober10,2012

©2012ProjectManagementInstitute.AllRightsReserved.

NotforDistributionorReproduction.

(Section 7.2.2.6) for these activities are aggregated into their associated work package costs. The

work package cost estimates, along with any contingency reserves estimated for the work

packages, are aggregated into control accounts. The summation of the control accounts make up

the cost baseline. Since the cost estimates that make up the cost baseline are directly tied to the

schedule activities, this enables a time-phased view of the cost baseline, which is typically

displayed in the form of an S-curve, as is illustrated in Figure 7-9.

Management reserves (Section 7.2.2.6) are added to the cost baseline to produce the

project budget. As changes warranting the use of management reserves arise, the change control

process is used to obtain approval to move the applicable management reserve funds into the cost

baseline.

Figure 7-8. Project Budget Components

PMBOK®Guide—FifthEdition

Pre‐ReleaseVersionOctober10,2012

©2012ProjectManagementInstitute.AllRightsReserved.

NotforDistributionorReproduction.

Figure 7-9. Cost Baseline, Expenditures, and Funding Requirements

7.3.3.2 Project Funding Requirements

Total funding requirements and periodic funding requirements (e.g., quarterly, annually)

are derived from the cost baseline. The cost baseline will include projected expenditures plus

anticipated liabilities. Funding often occurs in incremental amounts that are not continuous, and

may not be evenly distributed, which appear as steps as shown in Figure 7-9. The total funds

required are those included in the cost baseline, plus management reserves, if any. Funding

requirements may include the source(s) of the funding.

7.3.3.3 Project Documents Updates

Project documents that may be updated include, but are not limited to:

Risk register,

Activity cost estimates, and

Project schedule.

7.4 Control Costs

Control Costs is the process of monitoring the status of the project to update the project

costs and managing changes to the cost baseline. The key benefit of this process is that it

provides the means to recognize variance from the plan in order to take corrective action and

minimize risk. The inputs, tools and techniques, and outputs of this process are depicted in

Figure 7-10. Figure 7-11 depicts the data flow diagram of the process.

PMBOK®Guide—FifthEdition

Pre‐ReleaseVersionOctober10,2012

©2012ProjectManagementInstitute.AllRightsReserved.

NotforDistributionorReproduction.

Figure 7-10. Control Costs: Inputs, Tools & Techniques, and Outputs

Figure 7-11. Control Costs Data Flow Diagram

Updating the budget requires knowledge of the actual costs spent to date. Any increase to

the authorized budget can only be approved through the Perform Integrated Change Control

process (Section 4.5). Monitoring the expenditure of funds without regard to the value of work

being accomplished for such expenditures has little value to the project, other than to allow the

project team to stay within the authorized funding. Much of the effort of cost control involves

analyzing the relationship between the consumption of project funds to the physical work being

accomplished for such expenditures. The key to effective cost control is the management of the

approved cost baseline and the changes to that baseline.

Project cost control includes:

Influencing the factors that create changes to the authorized cost baseline;

Ensuring that all change requests are acted on in a timely manner;

PMBOK®Guide—FifthEdition

Pre‐ReleaseVersionOctober10,2012

©2012ProjectManagementInstitute.AllRightsReserved.

NotforDistributionorReproduction.

Managing the actual changes when and as they occur;

Ensuring that cost expenditures do not exceed the authorized funding by period,

by WBS component, by activity, and in total for the project;

Monitoring cost performance to isolate and understand variances from the

approved cost baseline;

Monitoring work performance against funds expended;

Preventing unapproved changes from being included in the reported cost or

resource usage;

Informing appropriate stakeholders of all approved changes and associated cost;

and

Bringing expected cost overruns within acceptable limits.

7.4.1 Control Costs: Inputs

7.4.1.1 Project Management Plan

Described in Section 4.2.3.1. The project management plan contains the following

information that is used to control cost:

Cost baseline. The cost baseline is compared with actual results to determine if a

change, corrective action, or preventive action is necessary.

Cost management plan. The cost management plan describes how the project costs

will be managed and controlled (Section 7.1.3.1).

7.4.1.2 Project Funding Requirements

Described in Section 7.3.3.2. The project funding requirements include projected

expenditures plus anticipated liabilities.

7.4.1.3 Work Performance Data

Described in Section 4.3.3.2. Work performance data includes information about project

progress, such as which activities have started, their progress, and which deliverables have

finished. Information also includes costs that have been authorized and incurred.

7.4.1.4 Organizational Process Assets

Described in Section 2.1.4. The organizational process assets that can influence the

Control Costs process include, but are not limited to:

Existing formal and informal cost control-related policies, procedures, and guidelines;

Cost control tools; and

Monitoring and reporting methods to be used.

7.4.2 Control Costs: Tools and Techniques

7.4.2.1 Earned Value Management

Earned value management (EVM) is a methodology that combines scope, schedule, and

resource measurements to assess project performance and progress. It is a commonly used

method of performance measurement for projects. It integrates the scope baseline with the cost

baseline, along with the schedule baseline, to form the performance baseline, which helps the

project management team assess and measure project performance and progress. It is a project

PMBOK®Guide—FifthEdition

Pre‐ReleaseVersionOctober10,2012

©2012ProjectManagementInstitute.AllRightsReserved.

NotforDistributionorReproduction.

management technique that requires the formation of an integrated baseline against which

performance can be measured for the duration of the project. The principles of EVM can be

applied to all projects in any industry. EVM develops and monitors three key dimensions for

each work package and control account:

Planned value. Planned value (PV) is the authorized budget assigned to scheduled

work. It is the authorized budget planned for the work to be accomplished for an

activity or work breakdown structure component, not including management reserve.

This budget is allocated by phase over the life of the project, but at a given moment,

planned value defines the physical work that should have been accomplished. The

total of the PV is sometimes referred to as the performance measurement baseline

(PMB). The total planned value for the project is also known as budget at completion

(BAC).

Earned value. Earned value (EV) is a measure of work performed expressed in terms

of the budget authorized for that work. It is the budget associated with the authorized

work that has been completed. The EV being measured needs to be related to the

PMB, and the EV measured cannot be greater than the authorized PV budget for a

component. The EV is often used to calculate the percent complete of a project.

Progress measurement criteria should be established for each WBS component to

measure work in progress. Project managers monitor EV, both incrementally to

determine current status and cumulatively to determine the long-term performance

trends.

Actual cost. Actual cost (AC) is the realized cost incurred for the work performed on

an activity during a specific time period. It is the total cost incurred in accomplishing

the work that the EV measured. The AC needs to correspond in definition to what

was budgeted in the PV and measured in the EV (e.g., direct hours only, direct costs

only, or all costs including indirect costs). The AC will have no upper limit; whatever

is spent to achieve the EV will be measured.

Variances from the approved baseline will also be monitored:

Schedule variance. Schedule variance (SV) is a measure of schedule performance

expressed as the difference between the earned value and the planned value. It is the

amount by which the project is ahead or behind the planned delivery date, at a given

point in time. It is a measure of schedule performance on a project. It is equal to the

earned value (EV) minus the planned value (PV). The EVM schedule variance is a

useful metric in that it can indicate when a project is falling behind or is ahead of its

baseline schedule. The EVM schedule variance will ultimately equal zero when the

project is completed because all of the planned values will have been earned.

Schedule variance is best used in conjunction with critical path methodology (CPM)

scheduling and risk management. Equation: SV = EV – PV

Cost variance. Cost variance (CV) is the amount of budget deficit or surplus at a

given point in time, expressed as the difference between earned value and the actual

cost. It is a measure of cost performance on a project. It is equal to the earned value

(EV) minus the actual cost (AC). The cost variance at the end of the project will be

the difference between the budget at completion (BAC) and the actual amount spent.

The CV is particularly critical because it indicates the relationship of physical

PMBOK®Guide—FifthEdition

Pre‐ReleaseVersionOctober10,2012

©2012ProjectManagementInstitute.AllRightsReserved.

NotforDistributionorReproduction.

performance to the costs spent. Negative CV is often difficult for the project to

recover. Equation: CV= EV − AC

The SV and CV values can be converted to efficiency indicators to reflect the cost

and schedule performance of any project for comparison against all other projects or

within a portfolio of projects. The variances are useful for determining project status.

Schedule performance index. The schedule performance index (SPI) is a measure of

schedule efficiency expressed as the ratio of earned value to planned value. It

measures how efficiently the project team is using its time. It is sometimes used in

conjunction with the cost performance index (CPI) to forecast the final project

completion estimates. An SPI value less than 1.0 indicates less work was completed

than was planned. An SPI greater than 1.0 indicates that more work was completed

than was planned. Since the SPI measures all project work, the performance on the

critical path also needs to be analyzed to determine whether the project will finish

ahead of or behind its planned finish date. The SPI is equal to the ratio of the EV to

the PV. Equation: SPI = EV/PV

Cost performance index. The cost performance index (CPI) is a measure of the cost

efficiency of budgeted resources, expressed as a ratio of earned value to actual cost. It

is considered the most critical EVM metric and measures the cost efficiency for the

work completed. A CPI value of less than 1.0 indicates a cost overrun for work

completed. A CPI value greater than 1.0 indicates a cost underrun of performance to

date. The CPI is equal to the ratio of the EV to the AC. The indices are useful for

determining project status and providing a basis for estimating project cost and

schedule outcome. Equation: CPI = EV/AC

The three parameters of planned value, earned value, and actual cost can be monitored

and reported on both a period-by-period basis (typically weekly or monthly) and on a cumulative

basis. Figure 7-12 uses S-curves to display EV data for a project that is performing over budget

and behind the schedule.

Figure 7-12. Earned Value, Planned Value, and Actual Costs

PMBOK®Guide—FifthEdition

Pre‐ReleaseVersionOctober10,2012

©2012ProjectManagementInstitute.AllRightsReserved.

NotforDistributionorReproduction.

7.4.2.2 Forecasting

As the project progresses, the project team may develop a forecast for the estimate at

completion (EAC) that may differ from the budget at completion (BAC) based on the project

performance. If it becomes obvious that the BAC is no longer viable, the project manager should

consider the forecasted EAC. Forecasting the EAC involves making projections of conditions

and events in the project’s future based on current performance information and other knowledge

available at the time of the forecast. Forecasts are generated, updated, and reissued based on

work performance data (Section 4.3.3.2) that is provided as the project is executed. The work

performance information covers the project’s past performance and any information that could

impact the project in the future.

EACs are typically based on the actual costs incurred for work completed, plus an

estimate to complete (ETC) the remaining work. It is incumbent on the project team to predict

what it may encounter to perform the ETC, based on its experience to date. The EVM method

works well in conjunction with manual forecasts of the required EAC costs. The most common

EAC forecasting approach is a manual, bottom-up summation by the project manager and project

team.

The project manager’s bottom-up EAC method builds upon the actual costs and

experience incurred for the work completed, and requires a new estimate to complete the

remaining project work. Equation: EAC = AC + Bottom-up ETC.

The project manager’s manual EAC is quickly compared with a range of calculated

EACs representing various risk scenarios. When calculating EAC values, the cumulative CPI and

SPI values are typically used. While EVM data quickly provide many statistical EACs, only

three of the more common methods are described as follows:

EAC forecast for ETC work performed at the budgeted rate. This EAC method

accepts the actual project performance to date (whether favorable or unfavorable) as

represented by the actual costs, and predicts that all future ETC work will be

accomplished at the budgeted rate. When actual performance is unfavorable, the

assumption that future performance will improve should be accepted only when

supported by project risk analysis. Equation: EAC = AC + (BAC – EV)

EAC forecast for ETC work performed at the present CPI. This method assumes

what the project has experienced to date can be expected to continue in the future.

The ETC work is assumed to be performed at the same cumulative cost performance

index (CPI) as that incurred by the project to date. Equation: EAC = BAC / CPI

EAC forecast for ETC work considering both SPI and CPI factors. In this

forecast, the ETC work will be performed at an efficiency rate that considers both the

cost and schedule performance indices. This method is most useful when the project

schedule is a factor impacting the ETC effort. Variations of this method weight the

CPI and SPI at different values (e.g., 80/20, 50/50, or some other ratio) according to

the project manager’s judgment. Equation: EAC = AC + [(BAC – EV) / (CPI × SPI)]

Each of these approaches is applicable for any given project and will provide the project

management team with an “early warning” signal if the EAC forecasts are not within acceptable

tolerances.

PMBOK®Guide—FifthEdition

Pre‐ReleaseVersionOctober10,2012

©2012ProjectManagementInstitute.AllRightsReserved.

NotforDistributionorReproduction.

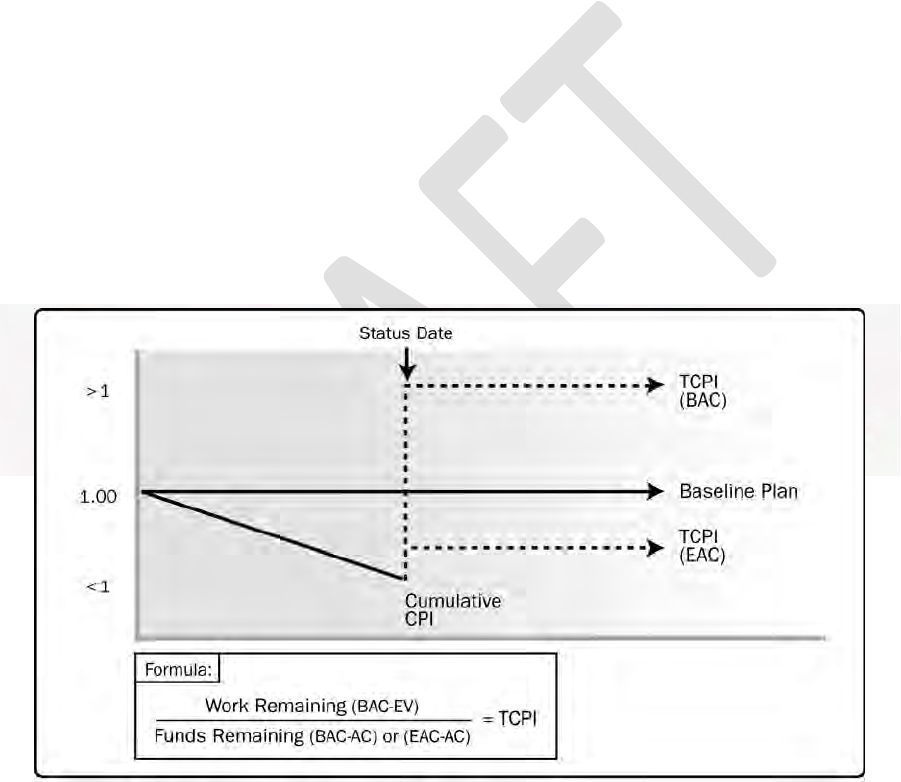

7.4.2.3 To-Complete Performance Index (TCPI)

The to-complete performance index (TCPI) is a measure of the cost performance that is

required to be achieved with the remaining resources in order to meet a specified management

goal, expressed as the ratio of the cost to finish the outstanding work to the remaining budget.

TCPI is the calculated cost performance index that is achieved on the remaining work to meet a

specified management goal, such as the BAC or the EAC. If it becomes obvious that the BAC is

no longer viable, the project manager should consider the forecasted EAC. Once approved, the

EAC may replace the BAC in the TCPI calculation. The equation for the TCPI based on the

BAC: (BAC – EV) / (BAC – AC).

The TCPI is conceptually displayed in Figure 7-13. The equation for the TCPI is shown

in the lower left as the work remaining (defined as the BAC minus the EV) divided by the funds

remaining (which can be either the BAC minus the AC, or the EAC minus the AC).

If the cumulative CPI falls below the baseline (as shown in Figure 7-13), all future work

of the project will need to be performed immediately in the range of the TCPI (BAC) (as

reflected in the top line of Figure 7-13) to stay within the authorized BAC. Whether this level of

performance is achievable is a judgment call based on a number of considerations, including risk,

schedule, and technical performance. This level of performance is displayed as the TCPI (EAC)

line. The equation for the TCPI based on the EAC: (BAC – EV) / (EAC – AC). The EVM

formulas are provided in Table 7-1.

Figure 7-13. To-Complete Performance Index (TCPI)

7.4.2.4 Performance Reviews

Performance reviews compare cost performance over time, schedule activities or work

packages overrunning and underrunning the budget, and estimated funds needed to complete

work in progress. If EVM is being used, the following information is determined:

Variance analysis. Variance analysis, as used in EVM, is the explanation (cause,

impact, and corrective actions) for cost (CV = EV – AC), schedule (SV = EV – PV),

PMBOK®Guide—FifthEdition

Pre‐ReleaseVersionOctober10,2012

©2012ProjectManagementInstitute.AllRightsReserved.

NotforDistributionorReproduction.

and variance at completion (VAC = BAC – EAC) variances. Cost and schedule

variances are the most frequently analyzed measurements. For projects not using

earned value management, similar variance analyses can be performed by comparing

planned activity cost against actual activity cost to identify variances between the cost

baseline and actual project performance. Further analysis can be performed to

determine the cause and degree of variance relative to the schedule baseline and any

corrective or preventative actions needed. Cost performance measurements are used

to assess the magnitude of variation to the original cost baseline. An important aspect

of project cost control includes determining the cause and degree of variance relative

to the cost baseline (Section 7.3.3.1) and deciding whether corrective or preventive

action is required. The percentage range of acceptable variances will tend to decrease

as more work is accomplished.

Trend analysis. Trend analysis examines project performance over time to determine

if performance is improving or deteriorating. Graphical analysis techniques are

valuable for understanding performance to date and for comparison to future

performance goals in the form of BAC versus EAC and completion dates.

Earned value performance. Earned value performance compares the performance

measurement baseline to actual schedule and cost performance. If EVM is not being

used, then the analysis of the cost baseline against actual costs for the work

performed is used for cost performance comparisons.

PMBOK®Guide—FifthEdition

Pre‐ReleaseVersionOctober10,2012

©2012ProjectManagementInstitute.AllRightsReserved.

NotforDistributionorReproduction.

Table 7-1. Earned Value Calculations Summary Table

PMBOK®Guide—FifthEdition

Pre‐ReleaseVersionOctober10,2012

©2012ProjectManagementInstitute.AllRightsReserved.

NotforDistributionorReproduction.

7.4.2.5 Project Management Software

Project management software is often used to monitor the three EVM dimensions (PV,

EV, and AC), to display graphical trends, and to forecast a range of possible final project results.

7.4.2.6 Reserve Analysis

During cost control, reserve analysis is used to monitor the status of contingency and

management reserves for the project to determine if these reserves are still needed or if

additional reserves need to be requested. As work on the project progresses, these reserves may

be used as planned to cover the cost of risk mitigation events or other contingencies. Or, if the

probable risk events do not occur, the unused contingency reserves may be removed from the

project budget to free up resources for other projects or operations. Additional risk analysis

during the project may reveal a need to request that additional reserves be added to the project

budget. Management and contingency reserves are addressed in more detail in Section 7.2.2.6.

7.4.3 Control Costs: Outputs

7.4.3.1 Work Performance Information

The calculated CV, SV, CPI, SPI, TCPI, and VAC values for WBS components, in

particular the work packages and control accounts, are documented and communicated to

stakeholders.

7.4.3.2 Cost Forecasts

Either a calculated EAC value or a bottom-up EAC value is documented and

communicated to stakeholders.

7.4.3.3 Change Requests

Analysis of project performance may result in a change request to the cost baseline or

other components of the project management plan. Change requests may include preventive or

corrective actions, and are processed for review and disposition through the Perform Integrated

Change Control process (Section 4.5).

7.4.3.4 Project Management Plan Updates

Elements of the project management plan that may be updated include, but are not

limited to:

Cost baseline. Changes to the cost baseline are incorporated in response to approved

changes in scope, activity resources, or cost estimates. In some cases, cost variances

can be so severe that a revised cost baseline is needed to provide a realistic basis for

performance measurement.

Cost management plan. Changes to the cost management plan, such as changes to

control thresholds or specified levels of accuracy required in managing the project’s

cost, are incorporated in response to feedback from relevant stakeholders.

7.4.3.5 Project Documents Updates

Project documents that may be updated include, but are not limited to:

Cost estimates, and

Basis of estimates.

PMBOK®Guide—FifthEdition

Pre‐ReleaseVersionOctober10,2012

©2012ProjectManagementInstitute.AllRightsReserved.

NotforDistributionorReproduction.

7.4.3.6 Organizational Process Assets Updates

Organizational process assets that may be updated include, but are not limited to:

Causes of variances,

Corrective action chosen and the reasons,

Financial databases, and

Other types of lessons learned from project cost control.

PMBOK®Guide—FifthEdition

Pre‐ReleaseVersionOctober10,2012

©2012ProjectManagementInstitute.AllRightsReserved.

NotforDistributionorReproduction.

8

PROJECT

QUALITY MANAGEMENT

Project Quality Management includes the processes and activities of the performing

organization that determine quality policies, objectives, and responsibilities so that the project

will satisfy the needs for which it was undertaken. Project Quality Management uses policies and

procedures to implement, within the project’s context, the organization’s quality management

system and, as appropriate, it supports continuous process improvement activities as undertaken

on behalf of the performing organization. Project Quality Management works to ensure that the

project requirements, including product requirements, are met and validated.

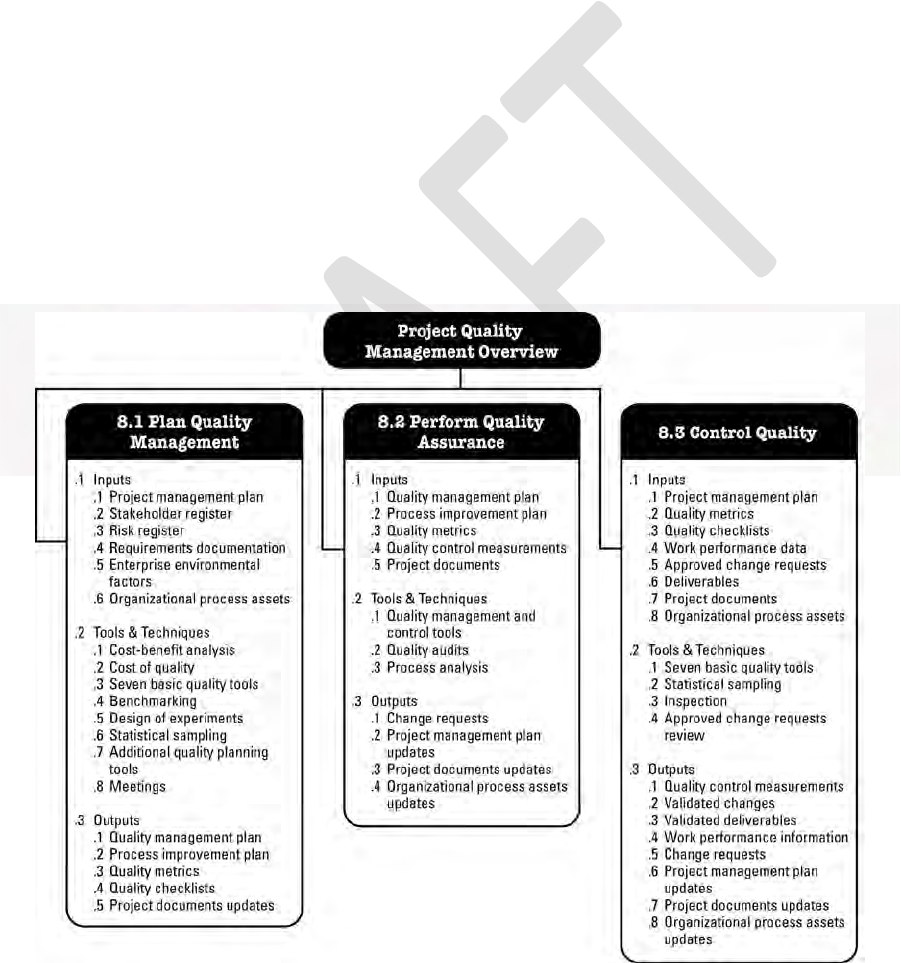

Figure 8-1 provides an overview of the Project Quality Management processes, which

include:

8.1 Plan Quality Management—The process of identifying quality requirements and/or

standards for the project and its deliverables and documenting how the project will demonstrate

compliance with quality requirements.

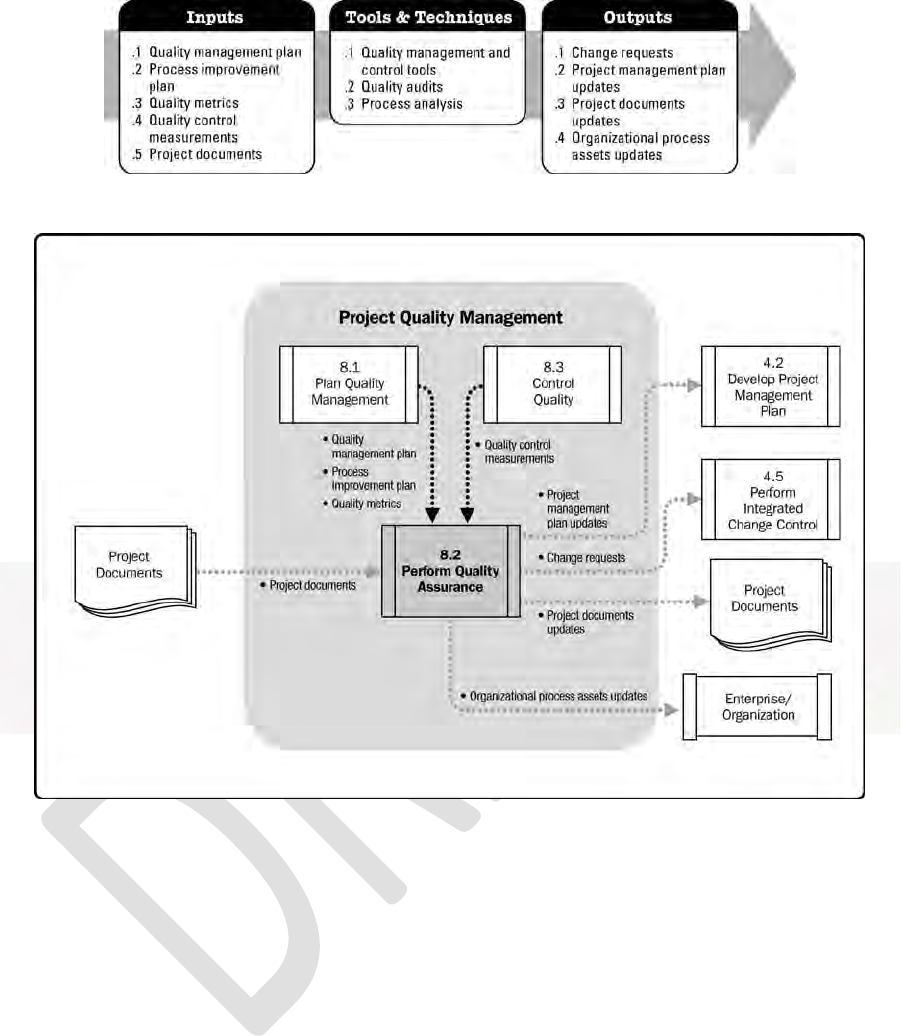

8.2 Perform Quality Assurance—The process of auditing the quality requirements and

the results from quality control measurements to ensure that appropriate quality standards and

operational definitions are used.

8.3 Control Quality—The process of monitoring and recording results of executing the

quality activities to assess performance and recommend necessary changes.

These processes interact with each other and with processes in other Knowledge Areas as

described in detail in Section 3 and Annex A1.

Project Quality Management addresses the management of the project and the

deliverables of the project. It applies to all projects, regardless of the nature of their deliverables.

Quality measures and techniques are specific to the type of deliverables being produced by the

project. For example, the project quality management of software deliverables may use different

approaches and measures from those used when building a nuclear power plant. In either case,

failure to meet the quality requirements can have serious, negative consequences for any or all of

the project’s stakeholders. For example:

Meeting customer requirements by overworking the project team may result in

decreased profits and increased project risks, employee attrition, errors, or rework.

Meeting project schedule objectives by rushing planned quality inspections may

result in undetected errors, decreased profits, and increased post-implementation

risks.

Quality and grade are not the same concepts. Quality as a delivered performance or result

is “the degree to which a set of inherent characteristics fulfill requirements. (ISO 9000)” Grade

as a design intent is a category assigned to deliverables having the same functional use but

different technical characteristics. The project manager and the project management team are

responsible for managing the tradeoffs associated with delivering the required levels of both

PMBOK®Guide—FifthEdition

Pre‐ReleaseVersionOctober10,2012

©2012ProjectManagementInstitute.AllRightsReserved.

NotforDistributionorReproduction.

quality and grade. While a quality level that fails to meet quality requirements is always a

problem, a low grade of quality may not be a problem. For example:

It may not be a problem if a suitable low-grade software product (one with a limited

number of features) is of high quality (no obvious defects, readable manual). In this

example, the product would be appropriate for its general purpose of use.

It may be a problem if a high-grade software product (one with numerous features) is

of low quality (many defects, poorly organized user documentation). In essence, its

high-grade feature set would prove ineffective and/or inefficient due to its low

quality.

The project management team should determine the appropriate levels of accuracy and

precision for use in the quality management plan. Precision is a measure of exactness. For

example, the magnitude for each increment on the measurement’s number line is the interval that

determines the measurement’s precision—the greater the number of increments, the greater the

precision. Accuracy is an assessment of correctness. For example, if the measured value of an

item is very close to the true value of the characteristic being measured, the measurement is more

accurate. An illustration of this concept is the comparison of archery targets. Arrows clustered

tightly in one area of the target, even if they are not clustered in the bull’s-eye, are considered to

have high precision. Targets where the arrows are more spread out but equidistant from the

bull’s-eye are considered to have the same degree of accuracy. Targets where the arrows are both

tightly grouped and within the bull’s-eye are considered to be both accurate and precise. Precise

measurements are not necessarily accurate measurements, and accurate measurements are not

necessarily precise measurements.

The basic approach to project quality management as described in this section is intended

to be compatible with that of the International Organization for Standardization (ISO) quality

standards. Every project should have a quality management plan. Project teams should follow the

quality management plan and should have data to demonstrate compliance with the plan.

In the context of achieving ISO compatibility, modern quality management approaches

seek to minimize variation and to deliver results that meet defined requirements. These

approaches recognize the importance of:

Customer satisfaction. Understanding, evaluating, defining, and managing

requirements so that customer expectations are met. This requires a combination of

conformance to requirements (to ensure the project produces what it was created to

produce) and fitness for use (the product or service needs to satisfy the real needs).

Prevention over inspection. Quality should be planned, designed, and built into—

not inspected into the project’s management or the project’s deliverables. The cost of

preventing mistakes is generally much less than the cost of correcting mistakes when

they are found by inspection or during usage.

Continuous improvement. The PDCA (plan-do-check-act) cycle is the basis for

quality improvement as defined by Shewhart and modified by Deming. In addition,

quality improvement initiatives such as Total Quality Management (TQM), Six

Sigma, and Lean Six Sigma could improve the quality of the project’s management as

well as the quality of the project’s product. Commonly used process improvement

models include Malcolm Baldrige, Organizational Project Management Maturity

Model (OPM3

®

), and Capability Maturity Model Integrated (CMMI

®

).

PMBOK®Guide—FifthEdition

Pre‐ReleaseVersionOctober10,2012

©2012ProjectManagementInstitute.AllRightsReserved.

NotforDistributionorReproduction.

Management Responsibility. Success requires the participation of all members of

the project team. Nevertheless, management retains, within its responsibility for

quality, a related responsibility to provide suitable resources at adequate capacities.

Cost of quality (COQ). Cost of quality refers to the total cost of the conformance

work and the nonconformance work that should be done as a compensatory effort

because, on the first attempt to perform that work, the potential exists that some

portion of the required work effort may be done or has been done incorrectly. The

costs for quality work may be incurred throughout the deliverable’s life cycle. For

example, decisions made by the project team can impact the operational costs

associated with using a completed deliverable. Post-project quality costs may be

incurred because of product returns, warranty claims, and recall campaigns.

Therefore, because of the temporary nature of projects and the potential benefits that

may be derived from reducing the post-project cost of quality, sponsoring

organizations may choose to invest in product quality improvement. These

investments generally are made in the areas of conformance work that act to prevent

defects or act to mitigate the costs of defects by inspecting out nonconforming units.

Refer to Figure 8-2 and Section 8.1.2.2. Moreover, the issues related to post-project

COQ should be the concern of program management and portfolio management such

that project, program, and portfolio management offices should apply appropriate

reviews, templates, and funding allocations for this purpose.

Figure 8-1. Project Quality Management Overview

PMBOK®Guide—FifthEdition

Pre‐ReleaseVersionOctober10,2012

©2012ProjectManagementInstitute.AllRightsReserved.

NotforDistributionorReproduction.

Figure 8-2. Fundamental Relationships of Quality Assurance and Control Quality to the IPECC,

PDCA, Cost of Quality Models and Project Management Process Groups

8.1 Plan Quality Management

Plan Quality Management is the process of identifying quality requirements and/or

standards for the project and its deliverables, and documenting how the project will demonstrate

compliance with relevant quality requirements. The key benefit of this process is that it provides

guidance and direction on how quality will be managed and validated throughout the project.

The inputs, tools and techniques, and outputs of this process are depicted in Figure 8-3. Figure 8-

4 depicts the data flow diagram of the process.

Figure 8-3. Plan Quality Management Inputs, Tools & Techniques, and Outputs

PMBOK®Guide—FifthEdition

Pre‐ReleaseVersionOctober10,2012

©2012ProjectManagementInstitute.AllRightsReserved.

NotforDistributionorReproduction.

Figure 8-4. Plan Quality Management Data Flow Diagram

Quality planning should be performed in parallel with the other planning processes. For

example, proposed changes in the deliverables to meet identified quality standards may require

cost or schedule adjustments and a detailed risk analysis of the impact to plans.

The quality planning techniques discussed here are those used most frequently on

projects. There are many others that may be useful on certain projects or in some application

areas.

8.1.1 Plan Quality Management: Inputs

8.1.1.1 Project Management Plan

Described in Section 4.2.3.1. The project management plan is used to develop the quality

management plan. The information used for the development of the quality management plan

includes, but is not limited to:

Scope baseline. The scope baseline (Section 5.4.3.1) includes:

o Project scope statement. The project scope statement contains the project

description, major project deliverables, and acceptance criteria. The product scope

often contains details of technical issues and other concerns that can affect quality

planning and that should have been identified as a result of the planning processes

in Project Scope Management. The definition of acceptance criteria may

significantly increase or decrease quality costs and therefore, project costs.

Satisfying all acceptance criteria that the needs of the sponsor and/or customer

have been met.

PMBOK®Guide—FifthEdition

Pre‐ReleaseVersionOctober10,2012

©2012ProjectManagementInstitute.AllRightsReserved.

NotforDistributionorReproduction.

o Work breakdown structure (WBS). The WBS identifies the deliverables and the

work packages used to measure project performance.

o WBS dictionary. The WBS dictionary provides detailed information for WBS

elements.

Schedule baseline. The schedule baseline documents the accepted schedule

performance measures, including start and finish dates (Section 6.6.3.1).

Cost baseline. The cost baseline documents the accepted time interval being used to

measure cost performance (Section 7.3.3.1).

Other management plans. These plans contribute to the overall project quality and

may highlight actionable areas of concern with regard to the project’s quality.

8.1.1.2 Stakeholder Register

Described in Section 13.1.3.1. The stakeholder register aids in identifying those

stakeholders possessing a particular interest in, or having an impact on, quality.

8.1.1.3 Risk Register

Described in Section 11.2.3.1. The risk register contains information on threats and

opportunities that may impact quality requirements.

8.1.1.4 Requirements Documentation

Described in Section 5.2.3.1. Requirements documentation captures the requirements that

the project shall meet pertaining to stakeholder expectations. The components of the

requirements documentation include, but are not limited to, project (including product) and

quality requirements. The requirements are used by the project team to help plan how quality

control will be implemented on the project.

8.1.1.5 Enterprise Environmental Factors

Described in Section 2.1.5. The enterprise environmental factors that influence the Plan

Quality Management process include, but are not limited to:

Governmental agency regulations;

Rules, standards, and guidelines specific to the application area;

Working or operating conditions of the project or its deliverables that may affect

project quality; and

Cultural perceptions that may influence expectations about quality.

8.1.1.6 Organizational Process Assets

Described in Section 2.1.4. The organizational process assets that influence the Plan

Quality Management process include, but are not limited to:

Organizational quality policies, procedures, and guidelines. The performing

organization’s quality policy, as endorsed by senior management, sets the

organization’s intended direction on implementing its quality management approach.

Historical databases; and

Lessons learned from previous phases or projects.

PMBOK®Guide—FifthEdition

Pre‐ReleaseVersionOctober10,2012

©2012ProjectManagementInstitute.AllRightsReserved.

NotforDistributionorReproduction.

8.1.2 Plan Quality Management: Tools and Techniques

8.1.2.1 Cost-Benefit Analysis

The primary benefits of meeting quality requirements include less rework, higher

productivity, lower costs, increased stakeholder satisfaction, and increased profitability. A cost-

benefit analysis for each quality activity compares the cost of the quality step to the expected

benefit.

8.1.2.2 Cost of Quality (COQ)

Cost of quality includes all costs incurred over the life of the product by investment in

preventing nonconformance to requirements, appraising the product or service for conformance

to requirements, and failing to meet requirements (rework). Failure costs are often categorized

into internal (found by the project) and external (found by the customer). Failure costs are also

called cost of poor quality. Figure 8-5 provides some examples to consider in each area.

Figure 8-5. Cost of Quality

8.1.2.3 Seven Basic Quality Tools

The seven basic quality tools, also known in the industry as 7QC Tools, are used within

the context of the PDCA Cycle to solve quality-related problems. As conceptually illustrated in

Figure 8-7, the seven basic quality tools are:

Cause-and-effect diagrams, which are also known as fishbone diagrams or as

Ishikawa diagrams. The problem statement placed at the head of the fishbone is used

as a starting point to trace the problem’s source back to its actionable root cause. The

problem statement typically describes the problem as a gap to be closed or as an

objective to be achieved. The causes are found by looking at the problem statement

and asking “why” until the actionable root cause has been identified or until the

reasonable possibilities on each fishbone have been exhausted. Fishbone diagrams

often prove useful in linking the undesirable effects seen as special variation to the

PMBOK®Guide—FifthEdition

Pre‐ReleaseVersionOctober10,2012

©2012ProjectManagementInstitute.AllRightsReserved.

NotforDistributionorReproduction.

assignable cause on which project teams should implement corrective actions to

eliminate the special variation detected in a control chart.

Flowcharts, which are also referred to as process maps because they display the

sequence of steps and the branching possibilities that exist for a process that

transforms one or more inputs into one or more outputs. Flowcharts show the

activities, decision points, branching loops, parallel paths, and the overall order of

processing by mapping the operational details of procedures that exist within a

horizontal value chain of a SIPOC model (Figure 8-6). Flowcharts may prove useful

in understanding and estimating the cost of quality in a process. This is obtained by

using the workflow branching logic and associated relative frequencies to estimate

expected monetary value for the conformance and nonconformance work required to

deliver the expected conforming output.

Figure8‐6.TheSIPOCModel

Checksheets, which are also known as tally sheets and may be used as a checklist

when gathering data. Checksheets are used to organize facts in a manner that will

facilitate the effective collection of useful data about a potential quality problem.

They are especially useful for gathering attributes data while performing inspections

to identify defects. For example, data about the frequencies or consequences of

defects collected in checksheets are often displayed using Pareto diagrams.

Pareto diagrams, exist as a special form of vertical bar chart and are used to identify

the vital few sources that are responsible for causing most of a problem’s effects. The

PMBOK®Guide—FifthEdition

Pre‐ReleaseVersionOctober10,2012

©2012ProjectManagementInstitute.AllRightsReserved.

NotforDistributionorReproduction.

categories shown on the horizontal axis exist as a valid probability distribution that

accounts for 100% of the possible observations. The relative frequencies of each

specified cause listed on the horizontal axis decrease in magnitude until the default

source named “other” accounts for any nonspecified causes. Typically, the Pareto

diagram will be organized into categories that measure either frequencies or

consequences.

Histograms, are a special form of bar chart and are used to describe the central

tendency, dispersion, and shape of a statistical distribution. Unlike the control chart,

the histogram does not consider the influence of time on the variation that exists

within a distribution.

Control charts, are used to determine whether or not a process is stable or has

predictable performance. Upper and lower specification limits are based on

requirements of the agreement. They reflect the maximum and minimum values

allowed. There may be penalties associated with exceeding the specification limits.

Upper and lower control limits are different from specification limits. The control

limits are determined using standard statistical calculations and principles to

ultimately establish the natural capability for a stable process. The project manager

and appropriate stakeholders may use the statistically calculated control limits to

identify the points at which corrective action will be taken to prevent unnatural

performance. The corrective action typically seeks to maintain the natural stability of

a stable and capable process. For repetitive processes, the control limits are generally

set at ±3 s around a process mean that has been set at 0 s. A process is considered out

of control when: (1) a data point exceeds a control limit; (2) seven consecutive plot

points are above the mean; or (3) seven consecutive plot points are below the mean.

Control charts can be used to monitor various types of output variables. Although

used most frequently to track repetitive activities required for producing

manufactured lots, control charts may also be used to monitor cost and schedule

variances, volume, and frequency of scope changes, or other management results to

help determine if the project management processes are in control.

Scatter diagrams, plot ordered pairs (X, Y) and are sometimes called correlation

charts because they seek to explain a change in the dependent variable, Y, in

relationship to a change observed in the corresponding independent variable, X. The

direction of correlation may be proportional (positive correlation), inverse (negative

correlation), or a pattern of correlation may not exist (zero correlation). If correlation

can be established, a regression line can be calculated and used to estimate how a