Consumer credit reports:

A study of medical and

non-medical collections

December 2014

2 CONSUMER FINANCIAL PROTECTION BUREAU

Table of contents

Table of contents......................................................................................................... 2

Executive summary ..................................................................................................... 4

Key findings ....................................................................................................... 5

1. Introduction—the reporting of collections tradelines ....................................... 8

1.1 Collections tradelines: a signal of financial distress and impact on credit

scores ........................................................................................................ 8

1.2 Concerns about furnishing practices of debt collectors ......................... 12

1.3 The special case of medical debt .............................................................15

1.4 Analysis of non-medical and medical collections tradelines on credit

reports ..................................................................................................... 16

2. The incidence and type of collections tradelines on credit reports ............... 18

3. Furnishing behavior of debt collectors ............................................................ 23

3.1 Diversity of collections furnishers .......................................................... 23

3.2 Variations in the timing of collections tradeline reporting ................... 25

3.3 Variations in tradeline persistence and fall-off ...................................... 27

3.4 Changes in status or balance of collections ............................................ 33

3.5 Account updating .................................................................................... 35

3.6 Furnishing as collections strategy .......................................................... 35

4. Medical collections tradelines ........................................................................... 38

3 CONSUMER FINANCIAL PROTECTION BUREAU

4.1 US Consumers’ medical payment obligations ........................................ 38

4.2 Consumer complaints to the CFPB about medical collections .............. 42

4.3 The profile of consumers with medical debt collections ........................ 43

4.4 Variability in medical collections tradeline incidence ........................... 48

4.5 Proposed new timing standards ............................................................. 49

5. Implications and conclusions............................................................................ 51

Appendix A: ............................................................................................................... 53

Consumer medical collections complaints ..................................................... 53

4 CONSUMER FINANCIAL PROTECTION BUREAU

Executive summary

When a debt is seriously delinquent and the creditor sells the debt or refers the debt either to a

collection agency or to an internal collection department, the collector or creditor can separately

report the account to one or more of the three largest nationwide consumer reporting agencies

(NCRAs) as an account in collections. The presence of a collections tradeline can have a negative

impact on a consumer’s credit score.

1

There are currently an estimated 220 million consumers with a credit report at one or more of

the NCRAs.

2

Collections tradelines affect the reports of nearly one out of three of these

consumers. Consumers are far more likely to dispute the accuracy of these tradelines than of

other information contained on their credit reports.

Roughly half of all collections tradelines that appear on credit reports are reported by debt

collectors seeking to collect on medical bills claimed to be owed to hospitals and other medical

providers. These medical debt collections tradelines affect the credit reports of nearly one-fifth

of all consumers in the credit reporting system.

This paper describes characteristics of the medical and non-medical collections tradelines on

consumers’ credit reports and the processes by which they appear and disappear. It draws on

analysis of data contained in the Consumer Financial Protection Bureau’s (CFPB) Consumer

1

‘Tradeline’ is defined as an entry by a credit grantor to a consumer’s credit history maintained by a credit reporting

agency. A tradeline describes the consumer’s account status and activity. Tradeline information includes names of

companies where the applicant has accounts, dates accounts were opened, credit limits, types of accounts,

balances owed and payment histories. In this report, “tradeline” refers to both active accounts and accounts

designated as collections. http://www.experian.com/credit-education/glossary.html.

2

Frequently Asked Questions on Credit Reports, Experian (Nov 25, 2014),

http://www.experian.com/ourcommitment/credit-report-faqs.html.

5 CONSUMER FINANCIAL PROTECTION BUREAU

Credit Panel (CCP); consumer complaints to the CFPB about collections; and interviews with

debt collection agencies, healthcare providers, and other observers of the healthcare billing and

payment processes. The CFPB has not sought to verify original research introduced in this paper

through its supervisory authorities. The paper does not draw upon supervisory information the

CFPB has learned through examinations it has conducted, and does not make conclusions about

whether any specific market participants are in compliance with particular statutes or rules

pertaining to consumer reporting.

Key findings

Collections tradelines affect many consumers. Nearly one-third of consumers with credit

reports (31.6 percent) have one or more collections tradelines on their credit reports. About 19.5

percent of credit reports - nearly one in five - contain one or more medical collections tradelines,

while 24.5 percent contain one or more non-medical tradelines.

Most collections tradelines result from unpaid bills rather than unpaid loans. Over

half are medical.

More than two-thirds of all collections tradelines (67.5 percent) – and over 80 percent of those

tradelines that can be attributed to a particular creditor or provider -- are reported on accounts

that originated with a healthcare provider, utility company, or telecommunications company.

These are companies that generally do not regularly report payment history to the NCRAs and

almost all rely on their collection agencies to report on accounts in collections. Medical

collections tradelines account for over half (52.1 percent) of all collections tradelines with an

identifiable creditor or provider.

Most collections tradelines are for small amounts. Medical collections tradelines

are even smaller than non-medical tradelines. The median unpaid non-medical

collections tradeline is $366 (with an average of $1,000). Medical unpaid collections tradelines

are even smaller with a median of $207 and average of $579. These contrast with the much

larger amounts that are due on credit cards or student loans that are seriously delinquent (more

than 120 or 150 days past due). Such accounts average several thousand dollars.

Information on collections tradelines are furnished to the three largest nationwide

consumer reporting agencies by a vast array of collectors. We can identify

approximately 1,400 different entities that furnish collections account information in our 5

6 CONSUMER FINANCIAL PROTECTION BUREAU

percent sample of credit reports. The degree of fragmentation varies significantly by the type of

debt in collections. Medical debt reporting is highly fragmented, with the top furnisher

accounting for only 3 percent of medical collections tradelines and the top 10 furnishers

accounting for only 18 percent of those tradelines. In contrast, the top furnisher for

telecommunications collections accounts for 37 percent of collections tradelines while the top 10

furnishers account for 83 percent of collections tradelines in that industry.

Third-party contingency collectors who furnish much of the collections tradeline

information have indirect and short term ties to the underlying debt. Third-party

collectors report information about their accounts in collections only during the time that they

are assigned the accounts by their creditor clients. Most of these tradelines appear on credit

reports when the account is assigned to the third party, and then disappear or “fall-off”the

report at the end of the assignment period. Rates of fall-off vary by collections type, with

medical debt having a lower fall-off rate than other types of collections tradelines. The large

number of collectors furnishing information on collections tradelines and their indirect

affiliation with the debt introduces potential sources of error in collections reporting.

Collections tradelines can represent a wide variety of consumer circumstances

when they appear on credit reports. There are no objective or enforceable standards that

determine when a debt can or should be reported as a collections tradeline. Creditors may elect

to sell a debt to a debt buyer or send a debt to a third-party collections agency or in-house

collections department at varying times in the collection cycle. Debt buyers and collectors

determine whether, when, and for how long to report a collections account as a collections

tradeline. Practices vary by type of account and within particular industries. Because of these

variations, there is only a limited relationship between the recency and severity or of a

delinquency and when or whether a collections tradeline appears on a consumer’s credit report.

Medical bills can be a cause of confusion and uncertainty and can result in

collections tradelines for consumers who are uncertain about what they owe, to

whom, when, or for what. The process of incurring medical expenses and the process by

which such expenses are turned into medical bills differs from recurring bills issued by

installment lenders, credit card companies, utilities, and telecommunications companies. Lack

of price transparency and the complex system of insurance coverage and cost sharing means

many consumers, including those who have health coverage, receive medical bills that are a

source of confusion. Among consumers who have submitted complaints to the Bureau about

debt collection problems, medical collections complaints are much more likely to be about the

7 CONSUMER FINANCIAL PROTECTION BUREAU

existence, amount, or information pertaining to the debt than non-medical collections

complaints.

A large portion of consumers with medical debts in collections show no other

evidence of financial distress and are consumers who ordinarily pay their other

financial obligations on time. 22 percent of consumers with collections tradelines (7

percent of all consumers with credit reports) have only medical collections tradelines. These

consumers owe less, have more available credit which they could use to repay their debt, and are

more reliable payers than consumers with non-medical collections tradelines or than consumers

with both types of collections tradelines. Indeed, of the consumers with only medical collections

tradelines, approximately 50 percent have otherwise “clean” credit reports with no indication of

serious past delinquencies.

Recently proposed rules and recently issued industry best practices pertaining to

medical billing and collections practices may help standardize the timing of when

collectors furnish information about medical debts in collections to the NCRAs.

These developments could reduce the number of medical collections tradelines that appear on

consumers’ records in situations in which the consumer is uncertain about what she/he owes, to

whom, and for what. These developments may also promise greater robustness in the way that

credit scores can interpret the presence of a medical collection tradeline on a credit report.

The Bureau will continue its efforts to assess the accuracy of information reported to and

contained on credit reports and to identify steps that various stakeholders can take to improve

the accuracy, integrity, and consistency of data in the system, consumers’ awareness of how the

system works, and consumers’ ability to make sure their credit reports accurately represent their

credit histories.

8 CONSUMER FINANCIAL PROTECTION BUREAU

1. Introduction—the reporting of

collections tradelines

1.1 Collections tradelines: a signal of

financial distress and impact on credit

scores

When a consumer falls behind on payments of a loan or other bill, the entity owed will ordinarily

make efforts to collect the amount due. During the early stages of delinquency, the effort may

consist of no more than a reminder notice or call about the outstanding obligation. As the length

of delinquency increases, so can the intensity of the collection activity. Eventually, the creditor

can refer the account to an in-house collections department, assign it to a third-party debt

collector, or sell the account to a debt buyer. Once the account is in collections, the creditor, debt

collector, or debt buyer can report the account to one or more of the three largest nationwide

consumer reporting agencies (NCRAs).

3

When this occurs, the account will appear on the

consumer’s credit report as an “account in collection,” referred to as a “collections tradeline” in

this paper.

Generally, the credit industry interprets the presence of a collections tradeline above a certain

minimum amount on a consumer’s credit report as a signal that the consumer is experiencing

3

These companies (TransUnion, Equifax, and Experian) are described in the Consumer Financial Protection

Bureau’s December 2012 white paper. See Consumer Financial Protection Bureau, Key Dimensions and Processes

in the U.S. Credit Reporting System: A review of how the nation’s largest credit bureaus manage consumer data

(September 2012) available at http://files.consumerfinance.gov/f/201212_cfpb_credit-reporting-white-paper.pdf.

9 CONSUMER FINANCIAL PROTECTION BUREAU

difficulty or reluctance in meeting his or her financial obligations.

When present, a collections

tradeline is incorporated as a derogatory factor in most credit scoring models, which use credit

report information to predict a consumer’s likelihood of repaying debts. For example, the Fair

Isaac Corporation (FICO) reports that for one of its recent scoring models (FICO 8), the addition

of any paid or unpaid collections tradeline of at least $100 to a consumer’s credit report will

reduce a score of 680 by over 40 points and a score of 780 by over 100 points.

4,5

Such a

significant drop in a credit score will generally increase a consumer’s cost of borrowing credit

and in some instances will preclude him or her from accessing the credit market.

In the Bureau’s representative sample of consumer credit reports, 9.1 percent of all tradelines

reported on consumer credit reports as of December 2012 were labeled as collections

tradelines.

6, 7

4

FICO develops and licenses the most widely used scoring models (although many other score models are used by

lenders), which typically generate scores ranging between 300 and 850 points. Other score developers also license

scoring models for use by lenders. For more information about the credit scoring market and scores used by

lenders, see Consumer Financial Protection Bureau, Analysis of Differences between Consumer- and Creditor-

Purchased Credit Scores at 3-4 (September 2012) available at

http://files.consumerfinance.gov/f/201209_Analysis_Differences_Consumer_Credit.pdf.

5

Letter from Fair Isaac Corporation (FICO), to authors (Oct.21, 2014) (on file with CFPB).

6

Data on the incidence and characteristics of collections tradelines on credit reports used in this study come from

the CFPB’s CCP. The CCP is a longitudinal, nationally representative sample of approximately 5 million de-

identified credit records from one of the NCRAs. The sample provides tradeline-level information for all of the

tradelines associated with each credit report or record each month, including collections debts of these consumers;

the record also includes a commercially-available credit score. The record-level information that is included in the

sample allows us to identify which debts reported by third-party collection agencies were from medical or non-

medical debts. While we can identify those collections that were from medical debt, nothing in the data reveals

information about the identity of the medical service provider(or consumer), the type of institution that provided

the service, or the nature of the services that were performed.

We analyze data from the CCP in two timeframes:

The first dataset depicts a snapshot of all consumer credit reports in the panel as of December 2012 for a random

sample of 4.95 million consumers and their corresponding 76.8 million tradelines. This dataset provides insight

into the incidence of collections tradelines, how frequently they appear on credit reports, and statistics on the sizes

and types of collections tradelines.

The second dataset is a time series depiction of approximately 234,000 collections tradelines that their respective

furnishers first reported on consumer reporting agency in January of 2013. (These tradelines may have been

10 CONSUMER FINANCIAL PROTECTION BUREAU

Not all accounts that become seriously delinquent end up being reported to the NCRAs as

collections tradelines. Some creditors simply choose not to furnish information about their

accounts, as the U.S. credit reporting system is a voluntary system. For entities that do opt to

furnish, NCRA guidelines define ways in which delinquencies can be designated.

8

Frequently,

for example, lenders who regularly furnish information about their borrowers’ accounts can

update the payment status information about an account to indicate that the payment is 30, 60,

90, 120 days (etc.) or more delinquent. The furnisher can also add a code indicating that it has

recognized a charge-off on the loan or debt.

9,10

Our research indicates that most credit card

issuers and student loan servicers furnish information about their seriously delinquent accounts

to the NCRAs using days delinquent to denote the severity of the delinquency. While the credit

card issuers and student loan servicers are likely to have assigned such accounts to a collection

agency or to an internal collections department of the creditor, these accounts do not appear as

separately designated collections tradelines on credit reports.

Among the 90.9 percent of accounts that were reported as active tradelines as of December 31,

2012, 2.1 percent of tradelines were at least 150 days past due and 3.6 percent of tradelines were

at least 120 days past due. A credit risk manager or credit scoring model can interpret an active

tradeline that appears this severely delinquent in similar ways to how they interpret a collections

recently been referred to a debt collector, or they may have been re-assigned by the creditor from one collector to

another or sold to a debt buyer. In the latter cases, the account may previously have appeared as a collections

tradeline furnished by another collector. The time series tracks these tradelines as first reported by furnishers and

then as they continue to appear on (or disappear from) credit reports in each of the subsequent months ending in

June, 2014. This sample provides visibility into the lifecycle of collections tradelines as they are reported by

individual furnishers. Because the panel does not identify original creditors associated with accounts in collections,

we are unable to easily track how these same collections tradelines were reported after they are reassigned from

one debt collector to another or sold by an original creditor to a debt buyer.

7

Under industry reporting guidelines, a “Collections Account” is described as “Account seriously past due/account

assigned to attorney, debt collection agency, or credit grantor’s internal collections department.”

8

The Consumer Data Industry Association (CDIA) provides guidance to debt collection agencies through its “Metro

2

®

” guidelines for furnishers to the NCRAs.

9

Charge-off is defined for the purposes of this report as a debt that is deemed uncollectible by the credit provider

and is subsequently written off. This type will be classified as 'bad debt expense' on the income statement, and

removed from the balance sheet.

10

We use the terms “furnish” and “furnisher” to refer respectively to the act of reporting consumer information to

one of these companies and to any entity that reports such information.

11 CONSUMER FINANCIAL PROTECTION BUREAU

tradeline: both are viewed as signals that the consumer can have serious difficulty and/or can

lack motivation in meeting his or her financial obligations.

Once an active account is closed, NCRA guidelines provide an alternative means by which the

account can be reflected on a credit report. At that point, the guidelines permit the account to be

reported as a collections tradeline. In addition, entities that do not regularly furnish information

on the status of their accounts – for example, utility companies or telecommunications

companies – can report a collections tradeline to the NCRAs after they have referred their

accounts to collections.

11

Debt collection agencies – when permitted or instructed by the

creditor – and debt buyers may also furnish information to the NCRAs about accounts on which

they are seeking to collect. When they do, the only reporting option permitted under the NCRA

guidelines is to report the accounts as collections tradelines.

This paper focuses on the account information that is furnished distinctly as collections

tradelines. While industry guidelines permit these accounts to be furnished by either creditors

or collectors, in practice, the vast majority of collections tradelines are furnished by third-party

debt collectors or debt buyers.

12

In our December 2012 snapshot of consumer credit report information, approximately 8.4

percent of collections tradelines appearing on credit reports are reported as paid in full or

settled for an amount less than the full balance. When a collections tradeline is recognized as

paid, the balance reported as owed is changed from an outstanding amount to zero.

13

Until

recently, most credit scoring models have recognized both paid collections tradelines and

unpaid collections tradelines above a certain minimal amount as indicators of financial difficulty

or unwillingness to pay on the part of the consumer.

11

A closed account may include indicators as to the reason for closure. Specific codes may indicate that an account

was discharged in bankruptcy, that it was sold to a debt buyer, or that it was paid and closed by the consumer.

When a furnisher reports an account as closed, it is not deleting the account (deletion is discussed later in this

paper). When an account is reported as closed, the associated tradeline may continue to appear on a credit report

as a closed account. In contrast, when a furnisher deletes a tradeline, information about the account will no longer

appear on the consumer’s credit report.

12

Industry interviews indicate that a small portion of collections tradelines are furnished by the original creditor,

however, we are unable to precisely quantify this share of all tradelines from the indicators contained in our

sample of credit report information.

13

According to Metro 2® guidelines, paid in full and settled accounts should not be deleted.

12 CONSUMER FINANCIAL PROTECTION BUREAU

Both unpaid and paid collections tradelines also represent derogatory information that is

subject to restrictions under the Fair Credit Reporting Act (FCRA) as to how long from the date

of the original delinquency the item is permitted to appear on most credit reports (seven years

for most debts and ten years for bankruptcies, after which the item must be omitted from the

report).

14

In our sample, 82.5 percent of the collections tradelines appear with an indicator designating

the industry from which the debt originated (17.5% were missing the industry designation).

Approximately two thirds (67.5 percent) of collections tradelines consist of debts owed to

utilities, telephone, wireless, and cable companies and amounts owed on medical bills.

15

Medical bills comprise approximately half of all collections tradelines.

1.2 Concerns about furnishing practices of

debt collectors

In the course of its market monitoring, supervisory, and consumer response activity, the CFPB

has sought to learn more about the accuracy, integrity, and consistency of information reported

to the NCRAs. Information from recent studies of credit report accuracy and from other sources

14

As per the Fair Credit Reporting Act, information excluded from credit reports include accounts placed for

collection or charged to profit and loss which antedate the report by more than seven years. The seven year period

“[…] shall begin, with respect to any delinquent account that is placed for collection (internally or by referral to a

third party, whichever is earlier), charged to profit and loss, or subjected to any similar action, upon the expiration

of the 180-day period beginning on the date of the commencement of the delinquency which immediately

preceded the collection activity, charge to profit and loss, or similar action.” Exemptions to these time limits are

found in 15U.S.C. §1681c (2012).

15

This statistic factors in the 17.5 percent of collections tradelines for which an original creditor classification may

be missing. If we excluded these unclassified items from the sample, the collections tradelines that originated with

a medical provider or with a utility, telephone, wireless, or cable company would represent 81.8 percent of all

collections tradelines in our sample.

13 CONSUMER FINANCIAL PROTECTION BUREAU

raise particular concerns about the accuracy and interpretation of collections tradelines, the vast

majority of which are furnished by debt collection agencies and debt buyers.

16,17,18

In its 2012 white paper on the U.S. credit reporting system, the CFPB reported (based on

interviews with the three largest NCRAs) that debts in collections accounted for 13

percent of tradelines in credit reports.

19

These tradelines however, accounted for nearly

40 percent of consumer disputes about inaccurate information handled by the NCRAs

through e-OSCAR, the online dispute system used by data furnishers and the NCRAs to

create and respond to consumer credit history disputes.

20

16

The Federal Trade Commission (FTC) found that 5 percent of consumer records had errors that could negatively

impact a consumer’s ability to get favorable loan terms. The study observed that one in four consumers (24

percent) identified what they believed to be an error on at least one of their three credit reports from an NCRA.

Among 1,001 consumers who reviewed their credit reports, collections tradelines accounted for 502 of 1,210

alleged inaccuracies identified by consumers regarding non-header information on their credit reports. Collections

tradelines accounted for 267 of 662 errors that were modified following consumer disputes regarding non-header

information.

17

Federal Trade Commission, Report to Congress under Section 319 of the Fair and Accurate Credit Transactions

Act of 2003 at 5, December 2012., available at

http://www.ftc.gov/sites/default/files/documents/reports/section-319-fair-and-accurate-credit-transactions-act-

2003-fifth-interim-federal-trade-commission/130211factareport.pdf.

18

The May 2011 study on credit reporting accuracy by the Policy and Economic Research Council (PERC) also found

similar results with small differences. For example, one in five credit reports (19 percent) were alleged by

consumers to have one or more potential inaccuracies on their records. In the PERC study, 1,970 potential

inaccuracies (potentially material and not material) were identified in the 3,876 reports examined. See Michael

Turner, Robin Varghese & Patrick D. Walker, PERC Results and Solutions, U.S. Consumer Credit Reports:

Measuring Accuracy and Dispute Impacts (2011) available at http://www.perc.net/wp-

content/uploads/2013/09/DQreport.pdf.

19

The percentage of all credit report tradelines we estimated to represent accounts in collection in our 2012 white

paper is larger than the 9.1 percent of tradelines we identify as collections tradelines in the Bureau’s CCP. The

2012 figure represents the average of responses to a question submitted to all three NCRAs regarding the

percentage of tradelines that represent accounts in collections; responses from the three NCRAs differed. In

addition, our question did not narrowly define an account in collection as narrowly as we do here (where we define

a collections tradeline as an account reported carrying a specific designation as defined in NCRA furnisher

guidelines). The 2012 figure may include accounts that are severely delinquent and may have experienced a

charge-off, but have not been furnished as collections tradelines.

20

Consumer Financial Protection Bureau, Key Dimensions and Processes in the U.S. Credit Reporting System: A

review of how the nation’s largest credit bureaus manage consumer data at 29 (September 2012) available at

http://files.consumerfinance.gov/f/201212_cfpb_credit-reporting-white-paper.pdf.

14 CONSUMER FINANCIAL PROTECTION BUREAU

The Federal Trade Commission’s (FTC) December 2012 accuracy study found that

collections tradelines accounted for 41 percent of the potential or alleged material errors

identified by consumers on their credit reports and 40 percent of errors that were

modified following disputes.

21

In addition, consumers who examined their credit reports

in conjunction with the FTC’s accuracy study had difficulty understanding how

collections were reported; collection agencies did not generally identify the specific

creditor or delinquent account that was involved.

22, 23

Again, the high error rate raises

concern about the underlying accuracy of collections reporting.

About 39 percent of consumer complaints received by the Bureau regarding collections

practices are about inaccurate information or inaccurate claims pertaining to the

account.

24

Of these, the most common complaint is that the consumer does not recognize

the debt as his or hers (see Section 4, Table 4F). These complaints suggest that either the

consumers are confused or mistaken about their accounts, or that the collectors are

collecting on the wrong consumer or amount. To the extent the latter is true, such

inaccuracies would presumably be incorporated into the information the collectors

furnish to the NCRAs.

Through its supervisory examinations of larger participants in the debt collections

industry, the Bureau found that one or more large collectors systematically failed to

investigate disputes from consumers received directly or through the NCRAs’ e-OSCAR

dispute handling system. In one example, the collector was simply removing the

tradeline referenced in the dispute entirely from the files it sent to the NCRAs, causing

the tradeline to be deleted from the consumers’ credit reports rather than conducting an

21

Federal Trade Commission, Report to Congress under Section 319 of the Fair and Accurate Credit Transactions

Act of 2003, December 2012., available at http://www.ftc.gov/sites/default/files/documents/reports/section-

319-fair-and-accurate-credit-transactions-act-2003-fifth-interim-federal-trade-

commission/130211factareport.pdf.

22

Id.

23

To the extent that information about the identity of the creditor associated with collections tradelines on a credit

report is unavailable, consumers will be more likely to dispute them as an error. See footnote 21.

24

This percentage was calculated by summing all collection complaints with the following codes: “debt is not mine,”

“debt was paid,” “attempted to collect wrong amount,” or “debt was discharged in bankruptcy.”

15 CONSUMER FINANCIAL PROTECTION BUREAU

investigation.

25

In February 2014, the CFPB published Bulletin 2014-01, confirming

furnishers’ obligation under the FCRA to conduct investigations of disputes they receive

from consumers.

26,27

In a public roundtable for industry and other stakeholders jointly hosted by the CFPB

and the FTC in 2013, participants acknowledged the general lack of standard record-

keeping practices used by debt collectors, debt buyers, and original creditors who assign

or sell collections accounts to these entities. The lack of standards regarding what

information is required to be present to substantiate a debt, and who is required to

maintain it, could also introduce variability or inaccuracy to the credit reporting system

when collectors or debt buyers furnish information about these accounts to the NCRAs.

28

These concerns about the accuracy of information furnished by debt collectors and their

treatment of disputes about the information carry particular weight given the negative impact

such information can have on the credit standing and credit scores of consumers.

1.3 The special case of medical debt

Medical debts comprise roughly half (52 percent) of the collections tradelines that appear on

consumer credit reports. Medical debts occur and are collected through unique circumstances

and practices that amplify concerns raised about collections tradelines generally. In particular,

the complexity of medical billing and the third-party reimbursement processes faced by most

25

Consumer Financial Protection Bureau, Supervisory Highlights at 13 (Spring 2014) available at

http://files.consumerfinance.gov/f/201405_cfpb_supervisory-highlights-spring-2014.pdf.

26

Consumer Financial Protection Bureau, Bulletin 2014-01, (2014) available at

http://files.consumerfinance.gov/f/201402_cfpb_bulletin_fair-credit-reporting-act.pdf.

27

A collections tradeline that contains potentially inaccurate information and that is simply deleted without an

investigation could result in same potential inaccuracy appearing in another tradeline on the consumer’s credit

report when the creditor reassigns the account to another debt collector. For further discussion about the impact

of reassignment, see Section 3.

28

Federal Trade Commission & Consumer Financial Protection Bureau, Roundtable on Data Integrity in Debt

Collection: Life of a Debt (2013), available at

http://www.ftc.gov/system/files/documents/public_events/71120/life-debt-roundtable-transcript.pdf.

16 CONSUMER FINANCIAL PROTECTION BUREAU

patients and their families is a potential source of confusion or misunderstanding between

patient, medical provider, and insurer. That complexity could lead some consumers to be

unaware of when, to whom, or for what amount they owe a medical bill or even whether

payment was the responsibility of the consumer rather than an insurance company.

While medical collections tradelines on credit reports appear as a result of circumstances that

differ significantly from other types of collections tradelines, credit scoring models have until

recently weighted such items identically to non-medical collections.

29

In a Data Point issued in

May 2014, the CFPB examined how medical tradelines reflect the creditworthiness of consumers

when compared to other types of collections tradelines. The report found that the presence of a

medical collections tradeline on a credit report is less predictive of future defaults or serious

delinquencies than the presence of a non-medical collections tradeline.

30

1.4 Analysis of non-medical and medical

collections tradelines on credit reports

This paper reflects findings from recent research by the CFPB to better quantify and understand

how and when medical and non-medical collections tradelines appear on credit reports. Our

research has involved analysis of data obtained from the CFPB’s CCP, review of consumer

complaints made to the CFPB pertaining to collections, interviews with collectors of medical and

29

According to FICO, medical collections are scored by the FICO 8 model the same as any other type of collection

on a consumer credit report. The company’s latest model, FICO 9, weights medical and non-medical collections

tradelines differently. Interview with FICO, in Washington, D.C. (Oct. 18, 2012).

30

The authors found that consumers with more medical than non-medical collections tradelines had comparable

delinquency rates to consumers whose scores were 8 to 10 points higher, but whose collections were mostly non-

medical. They also demonstrated that consumers with paid medical debt experienced delinquency rates that were

well below levels experienced by other consumers with the same scores whose medical collections were mostly

unpaid. This pattern of over-performance was consistent over the entire score range. Consumers with paid

medical debt were substantially over-penalized for their paid medical collections, with the median score

differential ranging between 16 and 22 points. See Kenneth P. Brevoort & Michelle Kambara, Data Point: “Medical

Debt and Credit Scores (May 2014), available at http://files.consumerfinance.gov/f/201405_cfpb_report_data-

point_medical-debt-credit-scores.pdf.

17 CONSUMER FINANCIAL PROTECTION BUREAU

non-medical debt and healthcare providers, and a review of literature on the medical billing and

collections process.

We present analyses from the CCP in Section 2 to characterize the incidence and types of

collections tradelines on credit reports. Section 3 discusses how collectors furnish the collections

tradelines found on credit reports, the diversity of furnishing behavior, and how this can reflect

the collectors’ relationship with original creditors.

Section 4 focuses on medical collections tradelines on credit reports, and some ways in which

consumers with medical collections exhibit different credit characteristics from consumers with

non-medical collections. This section draws on interviews with collectors and healthcare

providers to explore unique features of how medical debt arises and how it is collected and

reported.

Section 5 summarizes the implications of our research findings concerning collections tradelines

on credit reports and medical collections in particular. We discuss recent developments in credit

scoring models that could result in more precise and nuanced judgments regarding consumers’

creditworthiness based on the presence of collections tradelines, and ultimately benefit

consumers.

18 CONSUMER FINANCIAL PROTECTION BUREAU

2. The incidence and type of

collections tradelines on

credit reports

Approximately 220 million consumers’ credit activity is reflected on credit files maintained by

the three largest NCRAs.

31

In our sample of credit reports from one NCRA, collections tradelines

appear on the credit reports of almost one third (31.6 percent) of consumers.

The incidence of different types of collections tradelines on consumers’ credit reports in our

sample is depicted in Table 1.

32

Nearly one in five consumers (19.5 percent) has a credit report

containing one or more collections tradelines that originated with a medical provider.

33

Almost

one out of every four consumers (24.5 percent) has one or more non-medical collections

tradelines.

31

See footnote 2.

32

This study relies on guidance classifications provided to debt collection agencies and other furnishers by the CDIA

under its “Metro

®

” guidelines for furnishers to the NCRAs. These guidelines classify debt collections tradelines

into fifteen broad categories based on the original creditor’s type of business. We report the largest of these

business categories.

33

This estimate of the percentage of consumers affected and our subsequent estimate of the share of collections

tradelines on credit reports understate the impact of medical debt on consumers’ credit reports. Our analysis does

not account for or identify when a consumer has used a loan to pay medical bills. (For example, it is not

uncommon for consumers to pay for their medical bills using their credit cards.)

19 CONSUMER FINANCIAL PROTECTION BUREAU

TABLE 1: INCIDENCE OF COLLECTIONS TRADELINES

Collections tradeline type

Percentage of consumer credit reports

containing one or more collections

tradelines originating from…

Medical or health care 19.4%

Cable, cellular, wireless, other

telecommunications

8.7%

Utilities or energy 7.6%

Retail collections 6.9%

Banking 2.7%

Financial 1.5%

The non-medical collections tradelines that originated from telecommunication companies

(cable, landline, and wireless carriers) occur on 8.7 percent of credit reports; utilities (electric,

water, and gas companies) occur on 7.6 percent; and retail stores occur on 6.9 percent of

consumers’ credit reports. Collections tradelines from finance companies represent debts owed

primarily to non-auto and non-retail installment lenders; these were observed on 1.5 percent of

our sample of credit reports. Collections accounts originating from banking creditors (primarily

credit card accounts that are reported as collections tradelines) appeared on 2.7 percent of credit

reports.

34

Education collections tradelines, predominately made up of student loans, appeared

to affect less than 1 percent of consumers’ credit reports.

35,36

34

The low share of consumers who have certain types of collections tradelines on their credit reports (and the low

share of collections tradelines that are originated by certain types of creditors) may reflect differences in how some

collection agencies and lenders report accounts that are severely delinquent. Some lenders do not report accounts

that have been charged off and/or are in collections as collections tradelines to the NCRAs. For example, we

observed a low incidence of credit card accounts being reported as in collections. Preliminary CFPB research has

found that fewer than 17 percent of credit card accounts that have been charged off are reported as collections

tradelines; of these, third-party collection agencies furnish 16 percent and credit card lenders 1 percent. This

research indicates that most credit card accounts that have been charged off are reported by their original creditor

as active tradelines that are either in extended delinquency or as having been charged off. These accounts are not

counted among our estimate of total collections tradelines. Including seriously delinquent credit card accounts

20 CONSUMER FINANCIAL PROTECTION BUREAU

Most consumers whose credit reports contain collections tradelines have multiple collections

tradelines on their reports. The median consumer with collections tradelines has three such

tradelines (with an average of 4.5 collections tradelines) on his or her report. Among the 19.5

percent of consumers who have medical collections tradelines, the median consumer has two

such tradelines. Among the 24.5 percent of consumers who have non-medical collections

tradelines on credit reports, the median consumer has two such tradelines (and an average of

2.8).

Looking across all collections tradelines, more than half (52.1 percent) are associated with

medical providers. Figure 1 depicts the composition of all collections tradelines on credit reports

by creditor type.

that have not yet been charged off, or seriously delinquent or charged off student loan debt, would further increase

our estimate by an undetermined amount.

35

For defaulted federal student loans, there are alternatives to sending a tradeline to a collection agency. These

include withholding money from a consumer’s tax refund or other federal payments, wage garnishment, or federal

salary offset programs. Federal Student Aid Office, U.S. Department of Education available at

https://studentaid.ed.gov/repay-loans/default/collections.

36

Student loans that are severely delinquent appear to be similarly under-represented among collections tradelines.

We have not estimated the portion of such loans that are reported as active tradelines by their original creditors or

servicers.

21 CONSUMER FINANCIAL PROTECTION BUREAU

FIGURE 1: COMPOSITION OF COLLECTIONS TRADELINES ON CREDIT REPORTS BY TYPE OF CREDITOR

The collections tradelines observed in our sample are for small amounts, with a median amount

owed of $270 and an average of $781. Eighty-five percent of collections tradelines are for

amounts owed under $1,000.

37

A small number of very large unpaid collections tradelines

account for the majority of total dollars reported in collections. The largest 10 percent of

collections tradelines account for 61 percent of all dollars owed on collections tradelines, while

the largest one percent of collections tradelines account for 25 percent of total collections

amounts reported.

As Figure 2 indicates, the average and median amounts owed on collections; the amounts vary

considerably by type of creditor.

37

For some types of tradelines, the amount owed will reflect increases from the original balance of the debt owed,

when interest and fees accrue on the original debt. Increasing balances occur most frequently among finance

company accounts, where 48 percent these collections tradelines see regular increases in the monthly amount due.

52.1%

17.3%

8.2%

7.3%

7.2%

2.2%

1.6%

1.5%

1.2%

0.6%

0.4%

0.3%

0.1%

0.1%

0.1%

0.0%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

22 CONSUMER FINANCIAL PROTECTION BUREAU

FIGURE 2: AVERAGE AND MEDIAN AMOUNTS OF COLLECTIONS BY CREDITOR TYPE

Although many consumers in the sample have medical collections tradelines on their credit

reports, these debts often represent small amounts relative to the size of other types of debts.

The average amount of a medical collections tradeline is $579 with a median of $207. About 75

percent of all medical collections are under $490. Utilities and telecommunications collections

tradelines are similarly small.

38

In comparison, collections tradelines by finance companies

average $1,785 with a median of $515. Automotive collections tradelines average $5,587 with a

median of $3,995.

39

Overall, the average tradeline balance observed for all non-medical

collections was $1,000 and the median was $366.

38

These averages and medians are computed from all tradelines marked as collections tradelines. A few large

tradelines can be considered outliers. For example, removing the top 1 percent of medical collections tradelines in

our sample reduces the average amount of these collections tradelines to $315 from $579.

39

Collection industry interviews suggest automotive collections tradeline amounts represent deficiencies remaining

after vehicles have been repossessed by the creditor and the remaining debt has been assigned to a debt collector

or sold to a debt buyer.

$5,587

$3,174

$2,894

$2,620

$2,016

$1,785

$1,216

$1,082

$579

$538

$436

$417

$374

$299

$261

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

Median

Value

23 CONSUMER FINANCIAL PROTECTION BUREAU

3. Furnishing behavior of debt

collectors

The appearance of one or more collections tradelines above a minimum amount on a

consumer’s credit report has been viewed as a strong signal that the consumer may be

experiencing difficulty in meeting his or her financial obligations, but this signal can be

imprecise. As Section 2 suggests, collections tradelines can represent a diverse range of sizes and

types of accounts that have become delinquent. This section further describes ways in which the

appearance of collections tradelines can reflect diversity among debt collector furnishing

practices and of creditor strategies to collect on a debt.

3.1 Diversity of collections furnishers

Collection agencies that furnish information about debts in collections to the NCRAs are

numerous and diverse. In addition to variations in the size and in the types of accounts they

handle, collections furnishers can be either contingency collection agencies or debt buyers.

Contingency collection agencies are temporarily assigned responsibility for collecting by

the owner of that debt, typically the original creditor. These companies generally receive

a commission based on the number or amount of debts collected. Interviews with several

collection agencies indicate commission amounts can range from 10 percent to 40

percent of the collectedamount, depending on the type and age of the debt.

40

40

Telephone interviews with collection agencies, in Washington, D.C., various dates (on file with CFPB).

24 CONSUMER FINANCIAL PROTECTION BUREAU

Debt buyers purchase collections accounts from original creditors or other buyers at a

fraction of the face value of the total amount owed. Any amount collected above this

purchase price is then realized as net revenue. Debt buyers can collect for themselves,

rely on third-party collectors to pursue repayments, or enlist legal counsel to obtain

judgments in court.

Compared to furnishing by the financial firms that account for the majority of active tradelines

in credit reports, the furnishing of collections tradelines by debt collectors (both contingency

firms and debt buyers) is fragmented. The Bureau’s 2012 whitepaper on credit reporting found

that the 10 largest furnishers by tradeline count contributed more than half of all active

tradelines reported to the NCRAs.

41

In contrast, the largest furnisher of collections tradelines in

our national sample of credit reports is responsible for reporting only 4.7 percent of such

tradelines, and the top 10 furnishers for 22.1 percent. We can identify approximately 1,400

different entities that furnish collections account information.

42

The degree of fragmentation varies significantly by the type of debt in collections. Table 2

depicts the share of tradelines in our sample reported by the largest three furnishers and top 10

furnishers for major categories of debt. Medical debt reporting is highly fragmented, with the

top 10 furnishers accounting for only 18 percent of medical collections tradelines. In contrast,

the top 10 furnishers in the utilities, telecommunications, finance company, banking, and retail

industries account for between 59 percent and 83 percent of collections tradelines in those

industries.

41

Consumer Financial Protection Bureau, Key Dimensions and Processes in the U.S. Credit Reporting System: A

review of how the nation’s largest credit bureaus manage consumer data (September 2012) available at

http://files.consumerfinance.gov/f/201212_cfpb_credit-reporting-white-paper.pdf.

42

The Bureau estimates there are 4,500 debt collection agencies in the U.S.; however, we are unable to determine

from our sample of credit reports the percentage of these agencies that furnish to the NCRAs. See Defining Larger

Participants in Certain Consumer Financial Product and Service Markets, 77 Fed. Reg. 9592 (Feb. 17, 2012),

available at

https://www.federalregister.gov/articles/2012/02/17/2012-3775/defining-larger-

participants-in-certain-consumer-financial-product-and-service-markets#p-100

.

25 CONSUMER FINANCIAL PROTECTION BUREAU

TABLE 2: PERCENTAGE OF COLLECTIONS TRADELINES ATTRIBUTED TO TOP FURNISHERS BY TYPE

Collections

tradeline type

Top furnisher

tradeline share

Second largest

furnisher

tradeline share

Third largest

furnisher

tradeline share

Top 10

furnishers’

tradeline share

Medical/ Health

Care Collections

3.1% 2.5% 2.3% 18.3%

Cable, Cellular

and Wireless

Collections

36.9% 13.1% 12.3% 83.2%

Utilities and

Energy

Collections

32.4% 15.6% 3.5% 66.1%

Financial

Collections

36.2% 15.8% 4.6% 74.3%

Banking

Collections

29.7% 23.1% 22.3% 87.1%

Retail

Collections

20.7% 9.8% 7.0% 58.9%

3.2 Variations in the timing of collections

tradeline reporting

The first appearance of most collections tradelines on credit reports begins with the decision by

a creditor either to assign the debt to a third-party collector (and accord the collector

responsibility for furnishing to the NCRAs) or to sell the account to a debt buyer, which begins

furnishing information about the account. This decision can occur at a variety of different points

in the life of the account and stages of delinquency.

The creditor can choose to assign or sell the accounts at any stage of delinquency. In some cases,

the assignment can occur prior to charge-off. In some industries such as utilities or healthcare,

the timing of when a creditor can assign accounts to a third-party collector can be governed by

26 CONSUMER FINANCIAL PROTECTION BUREAU

state laws or regulations.

43

Industry interviews suggest that in the highly fragmented market for

medical collections where collections practices vary widely, assignment of unpaid medical bills

to third-party debt collectors can even occur when the bills are only 60 or even just 30 days past

due. Generally, when collectors furnish information to the NCRAs about these accounts, the

collections tradelines that result can represent delinquencies at a variety of stages.

There is similar variation in timing as to when a creditor chooses to sell an account to a debt

buyer. Industry interviews suggest that most sales to debt buyers only occur after an account has

been charged off by the original creditor. But sale - and subsequent furnishing of an account as a

collections tradeline by the buyer - can occur immediately after charge-off, or months or years

later.

Because of these variations, there is only a limited relationship between the severity or “recency”

of the delinquency and the timing a collections tradeline first appears on a consumer’s credit

report. NCRA guidelines instruct furnishers to include the date of first delinquency when

furnishing information about collections tradelines. This date should enable a user of a credit

report to determine the severity of delinquency of a collections tradeline when it first appears.

However, the date of first delinquency is not always available to the archived credit report

information that score developers use to develop and test their models. Some models therefore

can not take the date of first delinquency into account when determining the weight accorded a

collections tradeline in a consumer’s credit score.

44

43

One survey of a small sample of utility companies about their collections and credit reporting practices has found

that utilities vary considerably as to the stage of delinquency at which they transfer accounts to third-party

collection agencies and when those agencies pass on these delinquencies and defaults to the NCRAs. PERC:

“Credit Reporting Customer Payment Data: Impact on Customer Payment Behavior and Furnisher Costs and

Benefits;” 2009 at 17-19 available at http://www.perc.net/wp-content/uploads/2013/09/bizcase_0.pdf.

44

Not all NCRAs can provide the date of first delinquency in the archived data. It is the archived data that model

developers use to create credit scores.

27 CONSUMER FINANCIAL PROTECTION BUREAU

3.3 Variations in tradeline persistence and

fall-off

The variety of strategies creditors use when engaging collection agencies to recover or liquidate

defaulted debt is also reflected in variations in the duration of collections tradelines on credit

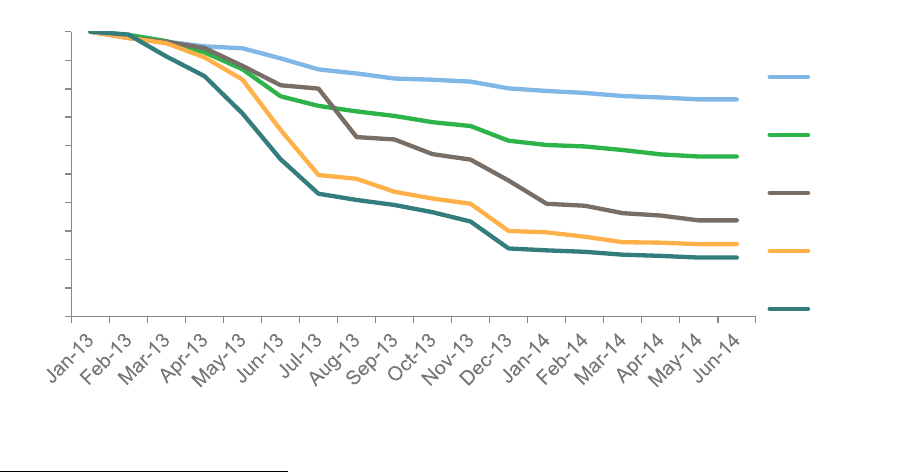

reports. Figure 3 illustrates the persistence of a single “vintage” of collections tradelines on

credit reports over an 18-month period.

45

The persistence of each tradeline varies by type of

account. For some types of accounts, most tradelines that first appeared at the beginning of the

observation period were no longer reported by the furnisher at the end of the period. The

observed fall-off was greatest among telecommunications, utilities, and retail tradelines.

46

FIGURE 3: PERSISTANCE OF FRESH COLLECTIONS TRADELINES BY TYPE

45

A “vintage” of credit accounts generally refers to accounts or loans that were originated at the same point in time.

Here we use the term “vintage” to refer to collections tradelines that first appeared on consumers’ credit reports at

the same point in time from a particular furnisher. Collections tradelines of the same vintage herein may

represent credit accounts that were originated at different points of time or became delinquent on different dates.

The particular vintage of accounts referred to in the analysis we describe first appeared as fresh collections

tradelines in January 2013 and were tracked through June 2014.

46

For the purposes of this study, we designate the term “fall-off”’ to mean that the tradeline disappeared from the

record during the 18-month period observed and was not aged off the record as per the maximum reporting time

allowed under the FCRA.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Banking/

finance

Medical

Retail

Utilities

Telecom

28 CONSUMER FINANCIAL PROTECTION BUREAU

We believe that re-assignment of accounts by creditors among multiple contingency collection

agencies explains most of the tradeline “fall-off” from the consumer’s record. Interviews with

collection agencies and other industry observers indicate that to maximize recoveries, many

creditors assign their delinquent accounts to a collection agency for a limited period of time and

then re-assign accounts from which the first agency has been unable to collect to a second

collection agency. As a result, the collectors first report information about these accounts to the

NCRAs at or after the beginning of the contract period during which their client creditors assign

them to collect on these accounts. Following the end of this assignment period, guidelines

published by the NCRAs require the collector to cease reporting and remove information on

these accounts from the NCRAs’ files. After the accounts have been re-assigned, the new

collection agency may begin reporting information about the accounts to the NCRAs, resulting

in a new collections tradeline appearing in the consumers’ credit report.

47

Some large creditors can have tiers of collectors: a primary tier to which it initially assigns a

portfolio of debts, a secondary tier of collectors to which it assigns debts after they have been

unsuccessfully “worked” for a period of time, and even a tertiary tier to which older debts are

assigned (if they are not eventually sold to a debt buyer).

We hypothesize that fall-off is relatively limited in the banking and finance industries because

many collections tradelines in these industries are reported by debt buyers. Historically, credit

card debts have accounted for the largest share of debt buyer purchases; these accounts are then

categorized as “banking’collections tradelines on credit reports.

48

These tradelines exhibited the

lowest occurrence of fall-off. This could reflect the tendency of these debt buyers to hold

purchased debts for long periods.

Fall-off of medical collections is relatively low when compared with other types of collections

tradelines. This can be explained by relatively low rates of debt reassignment by medical

providers. Interviews suggest that many medical providers choose not to manage multiple

47

The data contained in our sample of credit reports does not make it feasible to easily track tradelines that drop off

at the end of collections assignment periods and then re-appear when reported by a new collector. We have not

estimated what percentage of such tradelines reappear or what period of time typically transpires before they do.

48

Federal Trade Commission, The Structure and Practices of the Debt Buying Industry (2013), available at

http://www.ftc.gov/sites/default/files/documents/reports/structure-and-practices-debt-buying-

industry/debtbuyingreport.pdf.

29 CONSUMER FINANCIAL PROTECTION BUREAU

collector relationships. They tend to contract with a small number of contingency collectors

from which they do not subsequently re-assign their accounts.

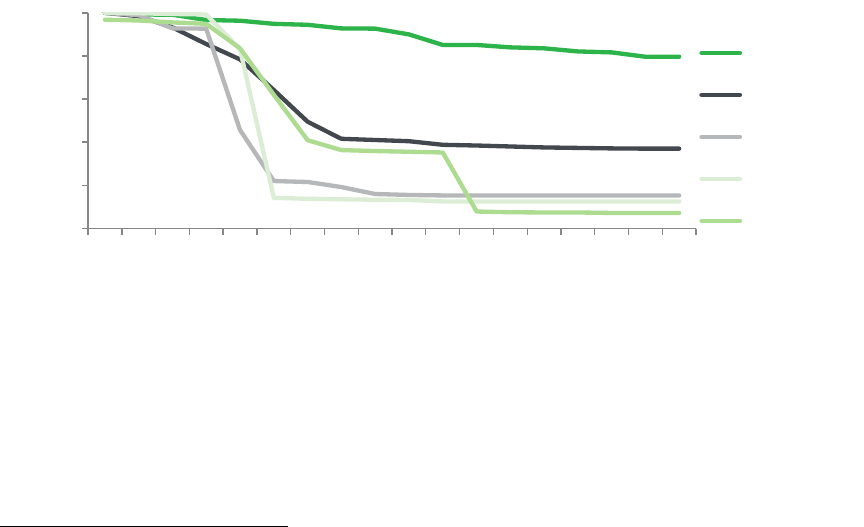

The impact of re-assignment is more evident when observing vintages of accounts from

individual furnishers. Figures 4-9 illustrates the January 2013 vintage of accounts reported by

the largest individual furnishers in the medical, telecommunications, banking, retail, utility, and

finance industries. Account fall-off within each of these industries is quite varied. In addition,

many of these accounts fall-off in steep “cliffs” that occur 3, 4, 6, or 12 months from the time

they first appear on the consumer’s record. These “cliffs” likely represent the end of assignment

periods.

49

Gradual slopes between cliffs, or in the absence of cliffs, can represent deletion of accounts over

time.

We hypothesize that this gradual fall-off can result from a combination of disputes from

consumers, aging off of debts that have exceeded the seven year obsolescence period and

deletion of some accounts after they have been repaid.

FIGURE 4: COLLECTIONS TRADELINE PERSISTANCE OF LARGEST FURNISHERS FOR MEDICAL

49

We also hypothesize that the large furnishers with gradual fall-off slopes and no cliffs may represent debt buyers

who collect on debts that they have purchased and who are not subject to assignment periods from creditors.

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

Jan-13

Feb-13

Mar-13

Apr-13

May-13

Jun-13

Jul-13

Aug-13

Sep-13

Oct-13

Nov-13

Dec-13

Jan-14

Feb-14

Mar-14

Apr-14

May-14

Jun-14

Furnisher A

Furnisher B

Furnisher C

Furnisher D

Furnisher E

30 CONSUMER FINANCIAL PROTECTION BUREAU

FIGURE 5: COLLECTIONS TRADELINE PERSISTANCE OF LARGEST FURNISHERS FOR TELECOM

FIGURE 6: COLLECTIONS TRADELINE PERSISTANCE OF LARGEST FURNISHERS FOR FINANCE

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

Jan-13

Feb-13

Mar-13

Apr-13

May-13

Jun-13

Jul-13

Aug-13

Sep-13

Oct-13

Nov-13

Dec-13

Jan-14

Feb-14

Mar-14

Apr-14

May-14

Jun-14

Furnisher A

Furnisher B

Furnisher C

Furnisher D

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

Jan-13

Feb-13

Mar-13

Apr-13

May-13

Jun-13

Jul-13

Aug-13

Sep-13

Oct-13

Nov-13

Dec-13

Jan-14

Feb-14

Mar-14

Apr-14

May-14

Jun-14

Furnisher A

Furnisher B

Furnisher C

31 CONSUMER FINANCIAL PROTECTION BUREAU

FIGURE 7: COLLECTIONS TRADELINE PERSISTANCE OF LARGEST FURNISHERS FOR RETAIL

FIGURE 8: COLLECTIONS TRADELINE PERSISTANCE OF LARGEST FURNISHERS BY BANKING

FURNISHERS

0%

20%

40%

60%

80%

100%

Jan-13

Feb-13

Mar-13

Apr-13

May-13

Jun-13

Jul-13

Aug-13

Sep-13

Oct-13

Nov-13

Dec-13

Jan-14

Feb-14

Mar-14

Apr-14

May-14

Jun-14

Furnisher A

Furnisher B

Furnisher C

Furnisher D

0%

20%

40%

60%

80%

100%

Jan-13

Feb-13

Mar-13

Apr-13

May-13

Jun-13

Jul-13

Aug-13

Sep-13

Oct-13

Nov-13

Dec-13

Jan-14

Feb-14

Mar-14

Apr-14

May-14

Jun-14

Furnisher A

Furnisher B

Furnisher C

32 CONSUMER FINANCIAL PROTECTION BUREAU

FIGURE 9: COLLECTIONS TRADELINE PERSISTANCE OF LARGEST FURNISHERS BY UTILITY

FURNISHERS

In recent interviews conducted during research on this paper, contingency collection agencies

stated that when they receive a request for validation from consumers under section 809 of the

Fair Debt Collection Practices Act or a dispute from consumers regarding the accuracy of

tradeline information under section 623 of the FCRA, they forward the request or dispute to the

original creditor.

50,51

During the dispute process, furnishers state that they remove the tradeline

from the consumer’s credit report until they can verify that the account is valid or that the

furnished information is accurate. We are not able to determine from our sample data whether

the firms or their client creditors conduct the required investigations under these statutes or, if

investigated and found to be correct, if the collector-furnishers re-report the validated or

corrected information. Nor can we determine or quantify the extent to which fall-off is

attributable to disputes or other causes.

50

15 U.S.C. § 1692g (2012).

51

15 U.S.C. § 1681s-2 (2012).

0%

20%

40%

60%

80%

100%

Jan-13

Feb-13

Mar-13

Apr-13

May-13

Jun-13

Jul-13

Aug-13

Sep-13

Oct-13

Nov-13

Dec-13

Jan-14

Feb-14

Mar-14

Apr-14

May-14

Jun-14

Furnisher A

Furnisher B

Furnisher C

Furnisher D

33 CONSUMER FINANCIAL PROTECTION BUREAU

3.4 Changes in status or balance of

collections

Consumer reporting industry guidelines instruct furnishers to report when a tradeline has been

paid in full or settled for less than the full balance by noting “paid” and indicating that the

balance owed is $0.

52

Our sample of collections tradelines that first appeared in January of 2013

indicates that the rates at which accounts are converted to “paid” varies considerably by account

type, as seen in Figure 10. While an average of 6.7 percent of collections tradelines are converted

to paid, this conversion rate can vary from 4.1 percent in the telecom industry to 11.8 percent in

the banking industry.

52

A “paid” status refers to collections tradelines that have been marked as “paid in full” or “settled for less than full

balance.”

34 CONSUMER FINANCIAL PROTECTION BUREAU

FIGURE 10: PAID OR SETTLED IN FULL RATES BY TYPE OF COLLECTIONS TRADELINE

The variations between account types in the rate of settlement partly reflects differences in the

effectiveness of collections efforts, which can in turn reflect differences in the nature of the debts

(for example, difference in the ages at which debts are sent to collectors between industries), or

differences across the consumers who owe these debts. The variation in settlement rates can also

reflect differences in furnishing practices across industries. NCRA reporting guidelines instruct

furnishers to continue to report collections accounts that have been closed and settled until the

FCRA obsolescence date has been reached

.53 54

However, our data do not allow us to assess how

consistently this requirement is being met by collections tradeline furnishers.

53

See footnote 13.

54

As per the Fair Credit Reporting Act, information excluded from consumer reports include accounts placed for

collection or charged to profit and loss which antedate the report by more than seven years. The seven year period

“[…] shall begin, with respect to any delinquent account that is placed for collection (internally or by referral to a

5.0%

7.4%

6.6%

4.1%

4.8%

11.8%

6.7%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

Retail Medical Utilities Telecom Finance Banking Average

Payment

Rate

Percentage of tradelines marked as paid or

settled

35 CONSUMER FINANCIAL PROTECTION BUREAU

3.5 Account updating

Industry guidelines for reporting to the NCRAs instruct furnishers to update information on all

accounts every month.

55

We observed that while most lenders furnishing data on active

tradelines observe this reporting standard, most collectors furnishing collections tradelines do

not.

During a six month period from December 2013 to June 2014, only a small fraction of medical,

utilities, and telecom collections tradelines were updated on a regular monthly basis. The

majority were never updated during this time period. In comparison, the large majority of active

(i.e. non-collections) tradelines are updated on a regular basis.

Furnishers of financial and banking collections accounts updated information of their tradelines

regularly. This updating behavior can relate to the fact that banking and finance items are

largely revolving or installment credit accounts that can be subject to ongoing interest and other

fees that collectors are permitted to accrue under state law and/or under the terms of the

original credit contract; furnishers of these items can be motivated to update on a regular basis

in order to maintain accurate information about the changing balances owned in the consumers’

files. It is unclear why medical, utilities, and telecom collections tradelines are not updated on a

monthly basis.

3.6 Furnishing as collections strategy

Furnishing information to the NCRAs can provide an incentive for borrowers or debtors to meet

their repayment obligations. Reporting derogatory information such as a collections tradeline

may motivate the consumer to contact the collection agency to resolve the debt, but could also

harm the consumer if the tradeline is reported without his/her knowledge, and/or if the

third party, whichever is earlier), charged to profit and loss, or subjected to any similar action, upon the expiration

of the 180-day period beginning on the date of the commencement of the delinquency which immediately

preceded the collection activity, charge to profit and loss, or similar action” 15 U.S.C. §1681c.

55

As per CDIA Metro 2

®

guidelines, third party collection agencies and debt buyers should update accounts as “in

collections” each month until the tradeline is paid. After payment, collections tradelines should be reported as

“account pain in full, was a collection account”.

36 CONSUMER FINANCIAL PROTECTION BUREAU

consumer did not have prior knowledge of the debt. Lack of prior knowledge can be more

prevalent in the case of medical debt due to the confusion caused by the medical billing process.

A collector may be most likely to resort to this tactic when the amount owed on a collections

account is small. Small dollar accounts are most often observed for telecommunications, utility,

and medical accounts. Attempts to make direct contact with the consumer via mail or telephone

to collect may not be cost efficient based on the odds of recovery and the amounts recovered.

Industry interviews have suggested that some collectors employ a strategy of “passive

collections” that involves reporting a debt in collections to the NCRAs and simply waiting for the

consumer to discover the tradeline (rather than actively seeking to collect from the consumer).

56

We cannot assess how often passive collections is used by collectors because we cannot

determine from our research whether the consumer was informed of the debt before the

collections tradeline was reported.

Whether or not a third-party collection agency reports to the NCRAs is generally a decision

made by the creditor that assigns accounts for collection. Some creditors instruct their collectors

to furnish. Others choose not to use furnishing as a collections strategy. Collectors told us in

interviews that not all of their clients permit them to furnish account information. And some

collectors whose clients have given them the option to furnish choose not to exercise that option.

The Healthcare Financial Management Association (HFMA) has stated that furnishing to a

consumer reporting agency is a common practice in the hospital industry.

57

However, we

interviewed several non-profit hospitals that do not allow their debt collectors to report to the

NCRAs because they believe this behavior can damage their reputations within the communities

they serve.

56

Telephone interviews with collection agencies, in Washington, D.C., various dates (on file with CFPB).

57

A 2005 HFMA survey shows that 83 percent of respondents (medical providers) report unpaid accounts to a

consumer reporting agency. Sixty-seven percent responded that they report unpaid accounts of any amount, 16

percent report unpaid accounts over a certain amount, 13 percent do not report unpaid accounts, and 4 percent

were unsure. Bureau interviews indicate that nearly all healthcare providers that permit reporting prefer to allow

their contracted collection agencies to report the unpaid accounts to credit reporting agencies as opposed to

reporting the unpaid accounts themselves. See Letter from Joseph Fifer, President and CEO Healthcare Financial

Management Association, to Internal Revenue Service (September 24, 2012) available at

www.hfma.org/WorkArea/linkit.aspx?LinkIdentifier=id&ItemID=5302.

37 CONSUMER FINANCIAL PROTECTION BUREAU

Whether or not certain creditors permit their debt collectors to furnish collections account

information to consumer reporting agencies may also be governed under state laws or

regulations that pertain to utilities or healthcare providers. Regardless of the reasons, the fact

that some collectors report while others do not introduces further variability into the

marketplace as to when collections tradelines appear or do not appear on consumers’ credit

reports.

In general, whether or not a collections tradeline appears on a consumer’s credit report, when it

appears or disappears, and whether it is labeled as paid or deleted when the account is settled,

all reflect furnishing policies and strategies of creditors and of the debt collection agencies and

debt buyers with which they do business. These practices can vary considerably and introduce a

range of variability that is not present in the reporting of active tradelines, for which payment

status (i.e., whether a payment is current, 30 days late, 60 days late, etc.) is the primary